Let’s look at the pension reform as it stands, however well or badly prepared it may be.

Currently, the reform, as presented by the Prime Minister, is both fair – it significantly improves the pensions of many people who receive little or no protection from the law or unions – and fully funded by age-based measures.

The issue of whether the reform should be solely “systemic” (or made universal, meaning a single system for everyone) rather than “parametric” (changing of the parameters to ensure balance) is a very surprising one. French people are much more worried about the amount of their future pensions than about whether the system is made universal, even though a universal system would be fairer.

This is probably where a lot of the mistrust is coming from: a points-based pension system may make people think that the system might be balanced by manipulating the value per point, and therefore the amount of the pensions paid, more particularly downwards. French people therefore needed to feel secure about their future pensions by being shown that the system would be safe-guarded, in other words funded.

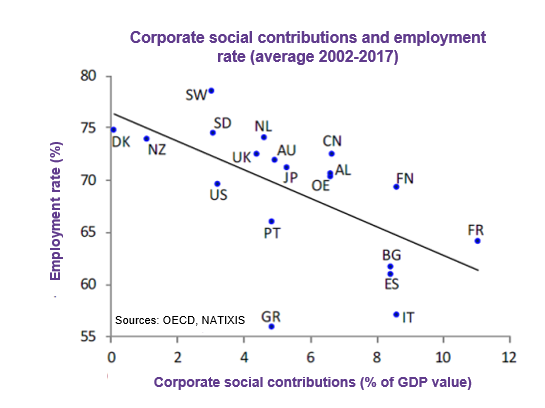

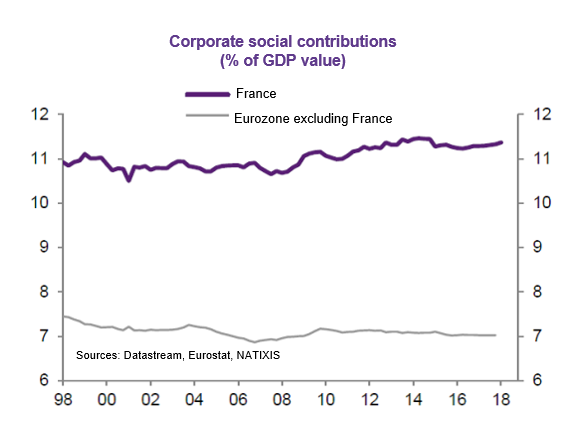

The only way of effectively ensuring that pay-as-you-go pension systems are balanced, without lowering pensions, is to adjust the length of people’s working lives, based on demographic changes. Otherwise, they can only be balanced by increasing employee and/or employer social security contributions. This would affect purchasing power and/or make the economy less competitive, immediately or at a later date, and so ultimately reduce the growth rate, employment and purchasing power in both cases. As companies in France already pay 60% higher social security contributions than companies elsewhere in the euro area, any further rise would be unacceptable, both socially and economically, as it would go against the interests of the French economy and of everyone working in it.

This leaves age-based measures as the only way of making the interests of current and future pensioners compatible with aiming for the highest potential growth for the economy. In France, in 1960, there were four taxpayers for every pensioner. In 2010, there were only 1.8 taxpayers per pensioner. At the same time, in 1958, the life expectancy at pension age was 15.6 years for women and 12.5 years for men. In 2020, this has increased to 26.9 and 22.4 years respectively. And the pension age is lower now than in 1958. The healthy life expectancy after retirement has also increased considerably.

Everyone understands this and expects the length of people’s working lives to change. Moreover, all of France’s neighbours have similarly raised their pension ages. We therefore also need to come to terms with reality so that our precious pay-as-you-go pension system is not endangered by an inability to fund it. In France, only around 30% of people aged 60 to 64 work, whereas in the other euro area countries nearly 50% work on average, with 57% in Germany and 68% in Sweden. Of course, work is not only necessary economically, it is also very often a means of integration, socialisation and self-fulfilment. Work also creates work in the dynamics of an economy, something that all the empirical studies have confirmed.

Now it must be considered whether it is better to establish a pivot age or to adjust the number of years worked, as this adjustment would take long careers and the strenuousness of the work more effectively into account, which would be fairer.

A good reform is one that is desirable and credible. This reform is desirable because it is fairer and because it gives French people greater security with regard to the amount of their future pensions. It is credible because it should be funded by adjusting the length of people’s working lives. It is desirable and credible if it does not increase social security contributions in France further, as they are already much higher than in other euro area countries.

For all these reasons, this reform will be positive and helpful for French people and the country’s economy.

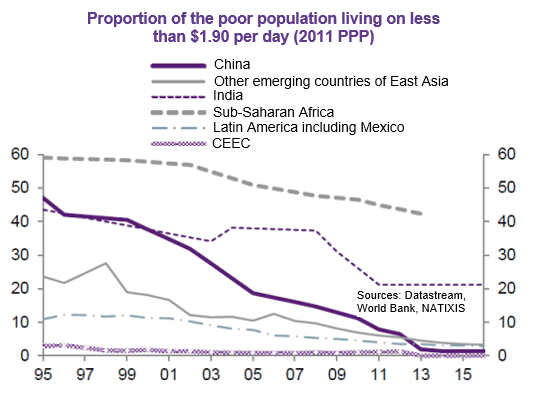

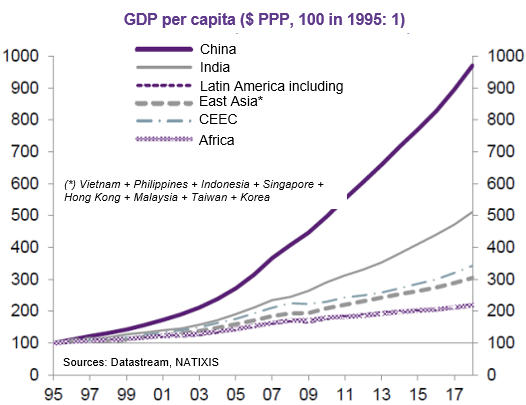

By nature, the topic of inequality covers several aspects. If we look at the global level, levels of inequality between poor and rich countries have decreased considerably since the 1980s. According to the World Bank, 40% of the world’s population in 1981 lived below the extreme poverty line compared with only 11% today. The growth rate of emerging countries has therefore substantially reduced inequalities between the average living standards of the various countries. And if we focus on just China and India, which have experienced and continue to see the strongest economic development since the 1980s, 2 billion people have risen above the poverty line. That’s great progress and one of the obvious benefits of globalisation.

That’s true not only for income, but also for health. My data are less recent, and it has improved even more since then. In 1940, life expectancy in developing countries was 44.5 years. In the 80s, it reached 64.3 years. That’s an increase of 20 years over this 40-year period. Meanwhile, people in developed countries are living nine years longer. Here again, we can see that inequalities in health and life expectancy have decreased.

On the other hand, inequalities within each country, whether developed or emerging, have increased on average with globalisation and growth. That’s because although the growth process allows the greatest number of people to increase their standard of living, some in each country are progressing faster than others, and in some countries, people at the top of the pyramid have access to a larger share of national income. The standard of living has therefore increased for nearly everyone. However, inequality has still managed to grow, simply because certain people’s situations have improved more quickly than others. That’s the nature of happiness, measured by economists in an informative way. All the studies show that happiness is relative. We’re happy when we’re doing better and when our situation improves faster than others. In other words, by comparison. In relative terms. So, even though everyone’s standard of living is rising, the increase in inequality is quickly becoming a social and political topic. We’re therefore seeing a phenomenon needing better clarity: dramatically smaller inequality between countries and growing inequality within countries, even though the level of wealth and well-being has increased overall.

The issue of inequality can therefore be addressed and analysed in various ways.

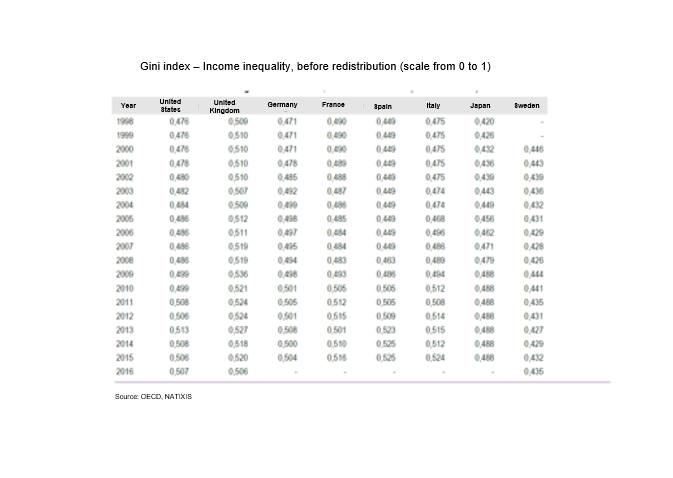

Income inequality can be measured by looking at the share of the country’s income held by the top 1%. Inequality can also be measured much more precisely and undoubtedly with more relevance with the Gini index. Gini was an economist and statistician who invented the method of studying the distribution of inequality across the entire population. We look at the differences between everyone two by two and average the differences from each to each. If the average of the differences is zero, that means that everyone has exactly the same income. An average of 1 means total inequality. These indices are measured across all OECD countries.

Lastly, a third way doesn’t look at income inequality but at inequality of opportunity. Of course, we’re talking about social mobility and the “poverty traps” that generations can fall into. Equal opportunity is obviously crucial because it relates to the republican pact, the social pact, and the ability to live together and obviously because it is fundamental for the health of a society and its cohesion. When inequality of opportunity is low, more people can be mobilised. That means that no matter where you’re born, if you have talent and equal opportunities, you’ll manage to advance. So, not only is the belief that everyone has the same opportunities an important factor of social cohesion, but it also helps to foster growth because it mobilises all talents wherever they are. The issue of inequality of opportunities is therefore crucial. It means knowing whether they are still the same and their children who all have their opportunities to succeed or if the pathways can be fluid without too much determination for the original social environment. And we’ll see that in France, there is a strong adhesion at both the top and the bottom.

Findings: I’ll start by presenting a few figures and then some analysis.

In France, compared with neighbouring countries, income inequality after distribution is rather low, whereas income inequality before distribution is rather high. Meanwhile, inequality of opportunities is rather high.

We’ll use these findings to try to come up with some possible conclusions in terms of economic policy and necessary reforms.

First, let’s take a look at the measurement of income inequality before distribution and after distribution. Before allocation, it’s clear, for example, that inequality is greater if wages range from 1 to 1,000 rather than 1 to 100. But we also have to consider people who aren’t working and therefore have very low incomes. The more people there are excluded from employment, the greater income inequality before redistribution is. And the more powerful the redistribution system is, whether through taxes, support income, and or other ways, the lower income inequality after distribution is.

Before distribution, the GINI index rose from 0.477 in the United States in 1996 to 0.507 in 2016. In the UK, contrary to what one might think, there has been little increase. It increased from 0.473 to 0.504 in the EU and from 0.409 to 0.488 in Japan. So, what do we see? Inequality has actually risen everywhere. And in the US, it hasn’t risen much more than elsewhere, before distribution. Its level of inequality isn’t really much higher than in the eurozone, while in Japan it’s lower.

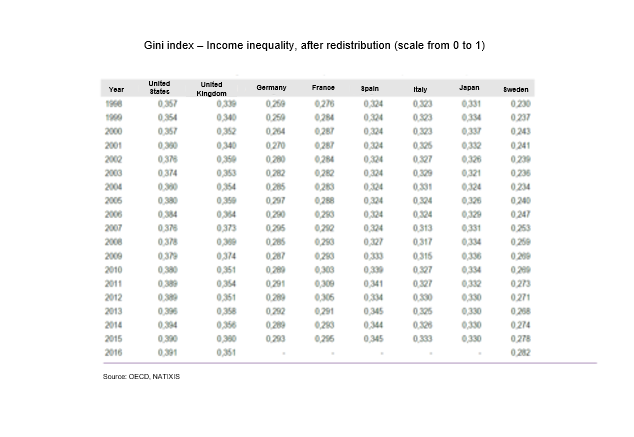

After distribution, the US fell from 0.507 to 0.391 in 2016. We can therefore see the effect of distribution. It clearly reduces income inequality. There has been a sharp decline in the UK as well. After distribution, the eurozone is a much more egalitarian system than the US since it’s much lower after distribution there. Europe therefore has a system that does more to reduce inequality. And Japan lies between them.

Let’s analyse France. Before redistribution, the Gini index rose from 0.490 in 1998 to 0.516 in 2015. That’s a fairly small upward trend in inequality. Are these inequalities big or small compared with other countries? In 2015, France was a little more unequal before redistribution than the US. Is it because there’s a broader range of wages? Of course not. It’s because there are many more people out of work. That’s an essentially French problem. Other countries very often have an employment rate 10 points higher (75% compared with 65% in France). Germany is almost at the US level. And we know that the unemployment level is very high there. Spain’s level of inequality before redistribution is even greater than France’s. Not surprisingly, Sweden is a more egalitarian country even before distribution. We can therefore see that France had high levels of inequality before redistribution.

But after redistribution, what’s the finding?

In 2015, France was at 0.295, one the lowest indices of all the countries considered. That means it went from having one of the highest indices in terms of inequality before redistribution to one of the lowest after redistribution. We can therefore see that redistribution is very strong in France. In the US, the level of inequality after redistribution is much higher than in France. But in Spain, Italy, and Germany, the level of income inequality after redistribution is about the same as in France. And France’s levels, again after redistribution, are quite comparable to Sweden’s.

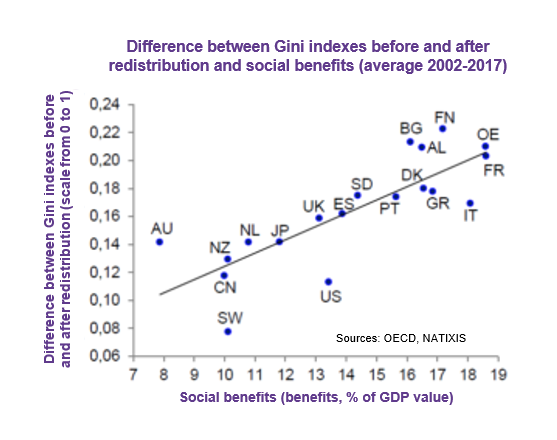

France thus has a one of the highest redistribution policies, relative to GDP, of all OECD countries. The advantage is reduced inequalities, but there are also disadvantages. It means much higher taxes and mandatory contributions, which is not without consequences. We can easily see a correlation between the Gini index after redistribution and the burden of social benefits relative to GDP. And, thanks to one of the strongest redistributions among OECD countries, France has one of the lowest income inequalities. Only Denmark, Finland, and Sweden have lower levels.

Now let’s consider the proportion of national income received by the 1% of individuals with the highest national income. In France, they received 9% of national income in 1995. In 2015, they received 10.5%. For the sake of comparison, Sweden had the lowest percentage at 6% of national income versus 9% in France in 1995 and 8% versus 10.5% in 2015. That’s not a huge difference. Let’s look at the United States. In 1995, the richest 1% received 15% of national income. In 2015, this figure was a little over 20%. That’s clearly a striking figure. It’s twice as much as in France. And the increase in the share received by the richest 1% has been much more brutal. In Germany, growth has been a little stronger than in France. While it was also 9% in 1995 like in France, it was 13% in 2015. However, we’re very far from the US. All in all, the richest 1% have received a growing portion of national income. But the phenomenon is much more visible in the US than in Europe.

Another way to analyse inequality is to look at the percentage of individuals at the poverty line.

The customary international way of calculating it can be called into question, but at least it’s an indicator used everywhere. We look at the median income of the French or Americans, for example, as a percentage. Anyone under 50%, or 60% like in our figures on this medium income, is considered poor. It is a relative notion of poverty.

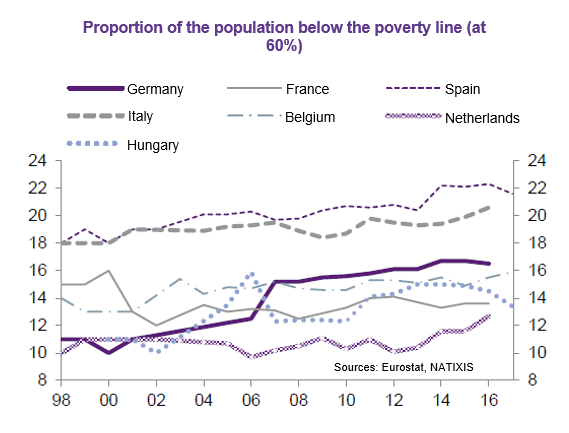

In France, few people are below the poverty line, meaning below 60% of French median income. Meanwhile the percentage is higher in Spain and Italy. It’s also higher in the US. And the percentage of the French population under the poverty line even decreased between 1998 and 2016. It increased in Germany over the same period. So, again, we can’t say that poverty is high or has increased in France. What we sometimes hear in the media is simply statistically false.

However, in France, inequality of opportunity is rather high compared with similar countries.

According to opinion polls conducted by the OECD, 44% of French respondents believe that education passed down by parents is important for progress through life. In the OECD, which includes Chile, Mexico, all European countries, the United States, etc., the average opinion is at 37%. This reflects a rather high sense of inequality of opportunity in France. Unfortunately, this opinion is correct. In France, socio-economic status is passed on more strongly than elsewhere from one generation to the next. The relative income level is passed on more strongly from one generation to another than in other countries. Lastly, the level of education and diploma is passed on more strongly from parents to children than in other countries. According to these three criteria, inequality of opportunity is greater in France than elsewhere.

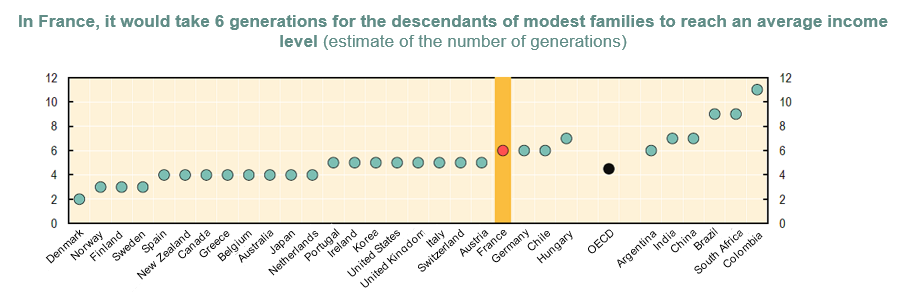

Of course, inequality of opportunity exists everywhere, since the socio-cultural environment is very important in the life and development of children. But the way we manage to partially correct the phenomenon can be more or less strong. The OECD calculated this and published a report on this subject, taking intergenerational mobility into account. Then we look at how many generations it takes for a family at the bottom of the ladder to reach the middle range. Clearly, the fewer generations required to reach the average, applying the average mobility of society, the less inequality of opportunity there is. The more generations it takes to achieve this, the more one is confined to the bottom of the ladder or symmetrically protected at the top of the ladder.

In Denmark, it takes 2 generations. In Norway, 3; in Finland, 3; in Sweden, 3; in Spain, 4. In New Zealand, Canada, Greece, Belgium, Australia, Japan, and the Netherlands, 4. In the United States, 5.And in France, 6.

Six generations so that someone at the very bottom of the income ladder has a chance that their great grandchildren will reach the middle income level, given French mobility. Germany doesn’t do better, and neither does Chile! And the average for the OECD is between 4 and 5.

Studies have reached the same conclusions about the inequality of opportunity in France, relative to comparable countries, by calculating the correlations between the income of parents and the income of children once they reach adulthood. The findings regarding correlations of diploma level are similar.

What structural reforms should be done to combat inequality of opportunity?

Of course, the reform of national education must be mentioned. There is currently much less mobility and equality of opportunity in France than many years ago when teachers who supported and pushed their deserving pupils were called “horsemen of the Republic”. This state of mind has not been abandoned, but it is much less widespread, and in reality, national education has declined in overall effectiveness for many reasons that can be explained more or less easily. The effectiveness of education is measured and compared using level tests carried out internationally by the OECD.

Comparative studies show that national education must be able to devote slightly more resources to children in disadvantaged areas or neighbourhoods. It’s also known that a lot comes into place early in life, in kindergarten, and in elementary school. That’s where more resources are needed. But let’s not fool ourselves. It’s a question of efficiency and not global means within national education in France, which has a much higher budget-to-GDP ratio than the other European countries for a disappointing result in the tests. People also must be supported during their career so that they can progress. Professional training in France is very inefficient and is in the process of being reformed.

Some countries do all this remarkably well, such as South Korea and the Nordic countries. They equip themselves with the means to ensure a good degree of social mobility in their country. Once again, that’s useful, not only for social cohesion, but also for the economy because there will be a search for talent that otherwise wouldn’t be able to express themselves and obviously contribute to the general growth.

In addition, long-term unemployment needs to be reduced, which means more effective support for returning to work and better incentives to take up a job. We also know very well that people in France are entitled to unemployment after four months of work. It’s one of the few countries where it takes so little time to be entitled to unemployment. That should be looked at. And, of course, we contributes to the creation of jobs must be facilitated…

It’s also important to work on territorial inequalities, because they exist.

So, there’s generally less social mobility in France than in other comparable countries, and this is reflected in the evolution between generations through income, degrees, and socio-professional categories.

Plus, we know that low mobility is not only intergenerational, but there is also fewer chances in France than elsewhere for people to be able to evolve during their life.

Two analyses:

From all this, I feel that there are two analyses that need to be given thought.

The first is the link between growth, innovation, and equal opportunities. The second is strong redistribution, which greatly reduces the initial inequalities that lead to a vicious circle.

First angle of analysis is the link between growth, equality, and innovation. For 20 years now, we’ve been living in a context of globalisation and a technological revolution related to digital. These two phenomena are increasingly eliminating repetitive work and the corresponding jobs.

Today, growing in an economy that is no longer a catch-up economy like in the post-war year requires being innovative. Innovation is crucial as the current driving force behind the growth of countries at the “technological frontier” (1). Emerging countries are catching up to developed countries, which must innovate constantly to continue to grow as emerging countries grow very quickly.

That means that we’re in an economy of knowledge and innovation – the only way to create growth and wealth.

As a result, we have to make sure to encourage innovation in our economy and our institutions (for example, organisational methods, labour market, and legislative framework). There’s also a link with equal opportunities because it’s obviously easier to fight poverty when there is growth. And it’s also easier to ensure social promotion to provide social mobility. If we step back and look at ourselves as a company rather than a country, we know that in a company that doesn’t develop, it’s very difficult to develop employees and help them grow. In a growing business, all those who are motivated and talented can be helped to grow.

Growth is therefore needed to reduce the inequality of opportunity and permit social promotion and mobility. If we don’t have enough growth and innovation, we end up with a blocked or jammed society and insufficient social mobility, and this leads to many social cohesion problems. In addition, as I already mentioned, the more we manage to promote equal opportunities, the greater the number of mobilised talents will be, and their energy will contribute to growth. So, we see the virtuous link between these different factors.

Plus, innovations create breakthroughs, which then create new sources of growth and wealth. Innovation therefore calls into question accrued benefits. And that’s also what enables social mobility. In the US, if we suddenly see people appear in the wealth rankings and develop new businesses very quickly, it’s because they seize innovations and can experience some amazing personal developments.

I’m not saying that this is a model in itself, but simply that, even at smaller scales, it’s essential. The more innovation, capacity to invest, and growth there are, the more it is possible to go beyond pensions and promote social mobility.

We therefore have to know how to ensure policies that facilitate innovation and promote this phenomenon. Once again, the innovation economy is the economy of knowledge: it’s education, it’s professional training, and it’s the promotion of all talents. It’s also means eliminating “poverty traps” by, as I already mentioned, better incentives to work, better support in finding a job, and easier abilities to switch jobs in shifting economies.

And that too is part of the necessary structural reforms. To encourage technical progress and innovation, competitiveness must also be encouraged through investment.

The second area of thought is the analysis of income inequalities before distribution and after distribution and the cost of this distribution (2).

The rather high income inequality before distribution is offset in France by redistribution, which is a strong redistribution because inequalities aren’t liked in France. In a way, what’s honourable is a collective choice. But a strong redistribution has a high cost in terms of social benefits and naturally social contributions and taxes. And because this leads to a lot of levies on companies, it spills over onto competitiveness. And lower competitiveness translates into fewer jobs. And the loop goes on. Because if there are fewer jobs, there are much stronger pockets of poverty and therefore large income inequalities before distribution. And then there’s long-term unemployment that must be offset by more redistribution and therefore more business costs. This leads us into a vicious circle.

The goal should therefore probably be to avoid over-repairing. Repairing is certainly normal, but better still is to do better upstream, to reduce income inequality before redistribution and avoid falling into this vicious circle. Prevent rather than repairing a lot of things.

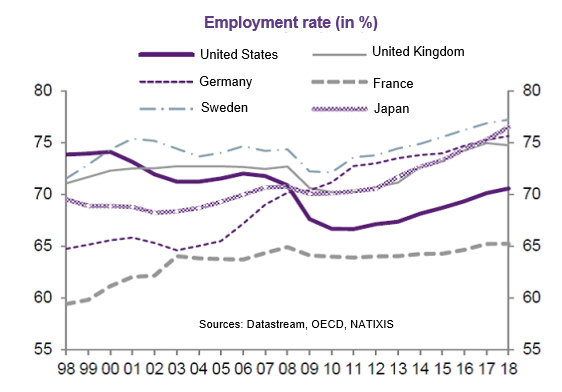

The employment rate in France is 65%. That’s around 10% lower than in comparable countries. This is an unacceptable situation in itself. In France, there aren’t enough working-age people who are working. If we consider the two extremes, between the ages of 60 and 65, there are far fewer people working in France than elsewhere. Much fewer than in Germany, not to mention Sweden, in comparing France to countries with comparable models. Similarly, it’s very difficult for young people to find a job. And we can see the correlation: the lower the employment rate is, the higher the social benefits needed to offset the created inequalities.

Now let’s consider the correlation between employment rates and the size of distribution policies. In other words, employment rates and differences between the GINI indices before and after distribution. France has the strongest redistribution policies and the lowest employment rates.

Again, the correlation is obvious for OECD countries. Because of France’s significant redistribution policy, its social security contributions are roughly 60% higher than the eurozone average and therefore the contributions of neighbouring and comparable countries.

Companies are therefore structurally less competitive. After social contributions, there are left with a considerable disadvantage in terms of the overall cost of labour. This then means a lack of jobs, resulting in large income inequalities before redistribution. Hence the fact that we redistribute strongly… I don’t think redistribution should be stopped. That’s not my point at all. But to do sound, normal redistribution that doesn’t cost in terms of growth and jobs, we must strive to allow many more people to work and therefore allow our businesses to be more competitive. Otherwise, we enter a vicious circle. Therefore, the challenge is to ensure that, even before redistribution, there are fewer inequalities because many more people are working. Taking action upstream to repair less means entering a virtuous circle, and this obviously means allowing many more people to work, resulting in less income inequality before redistribution and, at the same time, increasing equality opportunities. More working people means more self-sufficient people, far fewer pockets of poverty, and many more socialised people, because work is one of the main forms of socialisation.

Let’s hope that these figures and findings, sometimes unexpected because they are little-known, like these analyses, will be able to contribute to a useful debate about the effective reforms to be conducted, without preconceptions or confusion between the ultimate objective of reducing inequalities, with a primary focus on the high inequality of opportunities in France, and the means to be used to achieve it. In the words of Bossuet: “God laughs at men who complain of the consequences while cherishing the causes”.

(1) On this topic, see Schumpeterian growth theory by Philippe Aghion.

(2) – The analysis of the cost of redistribution and the vicious circle created between income inequalities before and after redistribution and the lack of competitiveness of French companies was developed by Patrick Artus in several ‘economic flashes’.

Corporations are beginning to be redefined in France, and with it, governance is as well. Shareholders remain at the centre of governance. Proper compensation for risks requires acknowledging their essential role. The question is knowing how to better integrate the interests of the other stakeholders in the company alongside them.

For a long time, this question was not raised. At Wendel, Renault, Michelin, etc. shareholders and board members were the same people, and often families. The original family capitalism did not have problems with governance by construction. But, to help them grow, companies opened up their capital, and through the stock market, offered shareholders the ability to sell their shares for liquid assets. The shareholder base became disparate, and its power over board members became diluted.

In the post-war era, managerial capitalism became the most prevalent practice. Board members were emancipated from shareholders and controlled the company on the basis of their “technical” knowledge. This created a technocracy. The interests of the two parties were no longer aligned. Board members sought corporate growth and continuity, inserting employees into organisational pyramids. But this configuration did not always lead to the best efficiency or profitability, creating conglomerates that were often heavy and lacking in agility, which too often neglected shareholder interests.

In the 1980s, alongside financial globalisation, shareholders reminded board members of their existence and of the priority of maximising wealth. This change translated into the creation of committees (audit, compensation and appointment, strategy, etc.) and the development of incentive mechanisms (bonuses, stock options, etc.), to align the interests of the board members with those of the shareholders. A whole series of indicators was imposed (return on equity, distribution rate, etc.), in the same way the doctrine of value creation was developed. And if results were not achieved, shareholders allowed “raids” that organised offensive power takeovers to optimise value, sometimes by cutting out previously established groups. In parallel, these various compensation tools based on the growth of corporate value promoted innovation by allowing “start-ups” to recruit talent that shared in the company’s risks when salaries alone were not enough to tempt them.

But shareholder capitalism rapidly reached its limits. Because expected financial yields seemed guaranteed, speculation often outweighed reasonable gambles. To meet minimum short-term profitability standards (15%, regardless of the activity sector and risk-free interest rate, in the 1990s and 2000s), many companies bought back their shares to strengthen their securities and/or increase their leverage ratio. Board member income experienced growth that was difficult to justify. In 1965, the average income of a CEO of a major American group was 44 times that of a worker. In 2000, it was 300 times the lowest salaries. Even more serious, in the face of expected yields that were disconnected from reality, we saw the appearance of unethical creative accounting: Enron, WorldCom, Parmalat and others even more recently. In some respects, subprimes and their consequences stem from the same phenomenon.

The crises of 2000-2003 and 2007-2009 resulted directly or indirectly from this, along with their shares of very significant economic and social costs.

Hence the need to address a new age in governance, that of true partenarial capitalism that is able to put the company’s clients, employees, and the environment, in particular, back alongside shareholders, in a model better adapted to ongoing commercial, behavioural, ethical, managerial, and technological revolutions.

Shareholders must always hold a central place as principals for board members. This is because, in theory, they assume the risk without any certainty of future yield. The practice has made shareholders partly protected against negative changes in the business context by partially spreading the risk to other corporate stakeholders: to employees, for whom variability of compensation or employment has increased; and to sub-contractors, whose margins for negotiation with their ordering customers have significantly weakened. Sometimes clients are also balancing items, through the lower product safety or accelerated obsolescence imposed on them. The climate is also affected by corporate choices.

Therefore, it must be possible to take better consideration of these stakeholders within a balanced governance framework, as they also share in the company’s risk, and because over the long term a company is responsible to all of them. Regulatory methods that help achieve the best compromises among them must guarantee sustainable and profitable development for the company.

For this reason, by the fact that their clients are owners and elected members of the boards of administration, by their decentralised model that strengthens close relationships not only with the clients they serve, but also with the territories in which they operate in symbiosis, and lastly by the attention and role they give to employees without sacrificing any of efficiency, cooperative or mutual banks represent an interesting possible form for redefining the company with expanded governance. It is up to them to take advantage of new technologies that would help further strengthen the validity of their model and modernity.

It is up to each type of company, listed, private, or cooperative, large or small, to reinvent the definition of the company and its governance, to make it a real partenarial organisation. The future of our open economies and democratic societies also depends upon this.

Aix en Provence Economic Conference (Rencontres économiques d’Aix en Provence) July 2017

The success of a currency area depends on the monetary policy which is implemented in it, but, more fundamentally, on the way it is organised. There are organisational modes and operating modes which facilitate or otherwise the creation of wealth and which we need to speak about here.

Firstly, when the eurozone was created it was to offer the citizens of the zone the possibility to share a single currency, which was a strong and very positive symbol for Europe. It was also to facilitate intra-zone exchanges because currency risk thus no longer existed. Yet we know that when we facilitate exchanges, we positively impact the growth rate. There was one final objective, that of displacing the external constraint of the borders of each country to the borders of the zone. It was a very important argument at the time. When you manage a series of highly interdependent countries and the external constraint is expressed at the borders of each country, you quickly encounter obstacles to growth. One country which has more need for growth than another, for example, because it has a stronger demographic, may experience a growth differential in its favour compared with its neighbours and partners and thus see its imports grow more than its exports.

Accordingly, it will rapidly encounter a current account balance deficit which is difficult to bear, which will limit its growth. This is what already happened to France, compared with Germany, before the eurozone. The idea that the external constraint in an optimal zone, in a complete monetary zone, is exercised at the borders of each country, obviously gives additional degrees of freedom to increase the overall growth level. The critical balance of the current account is that of the sum of the current account balances of the countries, some of which are positive and others negative. The principle of this is very interesting, therefore.

What happened in actual fact?

From 2002 to 2009-2010 we saw the per capita GDP of a large number of southern European countries catch up with the German per capita GDP. But nor can we fail to see that, since 2010, the difference has started to increase again. A few figures: in Portugal, the per capita GDP before the eurozone represented 50% of the German per capita GDP; it moved to 52-53% towards the mid-2000s, but it fell back to 48% in 2016. If I take a look at Greece, which is obviously an isolated case, it was 55% of German GDP in 2002, rose to 70% of German GDP but fell back well down on the level reached before the eurozone, to 42% in 2016. Spain was at 68%, it rose to 75%, then fell to 62%. Even Italy, which was at 88% – much closer to Germany ̶ rose to 90% in 2005, then fell to 72% in 2016. France was at 96% – very close, therefore, to Germany – it rose to 100%, but fell to 88% in 2016.

We can clearly see the effects of the creation of wealth linked to the creation of the eurozone, but also the recessionary effects of the eurozone’s specific crisis from 2010 onwards.

Where does this double movement come from? In fact, the conditions of the sustainability of the stronger growth of the southern European countries after the creation of the euro were not there. Why? Precisely because the organisation of the eurozone did not provide for the institutional arrangements permitting this sustainability. And this growth, in part, was achieved on credit simultaneously during this first period, so there was a very contrasted change in industrial production. We saw the zone’s northern countries grow their industrial production and a decline in the industrial production of the southern nations, including France. Obviously in a quite correlated way, even if the correlation is not total, we saw the current account balance move totally differently between Germany and the Netherlands, for example, which had a 2% GDP surplus before the eurozone and which rose to an 8% surplus over recent years, from 2008 onwards. Yet the eurozone excluding Germany and the Netherlands, went from a current account balance of 0% in 2002 to -6 % in 2008-2009. We thus have the northern countries which top the group, if I take the example of Germany and the Netherlands, at an average surplus of 8% of their current account balance, in 2008, whereas the others are posting a deficit of 6%! The difference is considerable and caused, for most of the southern European countries, a serious balance of payments crisis from 2010 onwards. The growth differential over the same period was not sustainable, therefore. Clearly, whereas a catch-up was occurring in terms of per capita GDP, other differences were being created. All this is largely due to intrinsic defects in the construction of the zone, but also to divergent structural policies of certain countries with respect to others.

One of the reasons for the eurozone’s major economic crisis between 2010 and 2012 is that we did not create a complete monetary zone and that we did not put in place coordination of economic policies, encouraging the wealthy countries to drive growth upwards and provide fresh impetus, thus alleviating the pain for those which had to slow down. This is a great shame but I think that there is no reason why we could never achieve this. Secondly, we have no mechanism for mutualising public debt or budgetary transfers from the countries doing the best to those doing less well, as is the case between states in the United States. In a single monetary zone, in principle, these mechanisms must exist which enable excessively strong asymmetric shocks to be avoided.

In addition, upstream, due to structural policies not having been put in place by the southern European counties, the creation of the eurozone, of the single currency, has facilitated a dynamic of industrial polarisation to the benefit of the northern countries. Industrial production has partially moved to the countries which were the strongest industrially and which have thus accentuated their advantages, favoured by the creation of the eurozone. This was not done without efforts on their part, since they accentuated their advantages thanks to their structural reforms, but also thanks to the eurozone mechanics. Investments spontaneously move to where physical and institutional infrastructure (production conditions, networks of subcontractors, training, job market, etc.) are the most favourable whereas there is longer a currency risk between these countries. No more need to invest as much in production in certain southern European countries since the fear of being able to sell less in the event that they devalued their currency is gone. Moreover, since currency adjustments are no longer made, if we have no policy to help with convergence, the following phenomenon occurs: we give a bonus to the countries which are the strongest and which no longer incur the readjustment of competitiveness by the devaluation of the currencies of the other countries. This is the equivalent of a regular under-evaluation, of Germany in reality, over time.

The economic crisis of the southern countries, caused notably by this partial deindustrialisation, which has greatly contributed to the crisis in their balance of payments, has also been largely due to the single monetary policy which has resulted in creating an interest rate which corresponded to the requirements of the average of the countries in the zone and which, for this reason, for the countries which were growing the fastest and catching up, has given too low interest rates which has meant facilitating the development of, in particular, real estate bubbles or credit bubbles, very visible in certain countries, which later burst.

All this has been reinforced by the fact that the financial markets failed during the period, as from 2002 to 2009 there was no self-regulation of the long interest rates which, despite the circumstances described above, constantly converged towards the German interest rates, the lowest in the eurozone. Accordingly, the countries which constantly increased their overall debt level or their current account balance deficit, did not get a wake-up call. If the markets had worked correctly, their interest rates should have increased to ring the necessary alarm bells to ensure that countries regulate themselves better and limit their external debt and their current account balance deficit.

In fact, the lack of balanced and symmetrical adjustment mechanisms shared by all the eurozone countries, the lack of sufficient institutional arrangements (such as the coordination of the economic policies, the absence of budgetary transfers, etc.), but also the lack of structural reforms in each of the southern countries constituted the basis of the crisis which erupted in 2010. As previously explained, this was a classic balance of payments crisis, a sudden stop of the southern countries. With a stop to the mobility of private capital which stopped being poured into the southern countries whereas they were doing so naturally before that from the northern countries, which, symmetrically, experienced current account surpluses. This caused asymmetric adjustments. These countries, which did not have not the above-mentioned institutional arrangements which would have been opportune available to them, had but one possibility: to adjust downwards in isolation. By reducing their employment and social costs, by reducing their production costs, thus by implementing austerity policies, in order to reduce their imports on the one side – when demand is reduced, imports are automatically reduced – and on the other still reducing costs, by regaining competitiveness to drive their exports back up. This obviously has a high social cost and a very important political cost.

In conclusion it must be said, very fortunately, that the ECB saved the eurozone in 2012. It saved it because the ECB ended the vicious circles that had become rooted in it and which were having catastrophic effects. The vicious circle between the nations’ debt and interest rates. Interest rates which were going sky high, were increasing even further the weight of the nations’ debt, which were leading in turn to a further increase in interest rates. The ECB also interrupted the second vicious circle which existed between the nations’ public debts and the banks of the countries concerned. Since the banks held the nations’ securities, the banks increased the perceived risks as to their solvency, since the nations were in bad shape. But as the nations were obliged to refinance or recapitalise the banks, they seemed at greater risk themselves. The ECB, by various appropriate measures and stances, saved the eurozone.

But the ECB cannot permanently – and it says it itself very clearly – be the only one to bear all the efforts. It does so remarkably, but it does so to buy time from governments which have to do two things, which is also rightly and incessantly repeated by the central bank. For the southern European countries and France, structural reforms must be carried out because it is this which bring the extra potential growth and will facilitate their solvency trajectory. Germany will make no efforts if the other countries do not make structural reforms because, from its point-of-view, there is no reason to show solidarity with countries which would not make the necessary efforts to avoid being in a position to repeatedly call for aid. This is a crucial factor. At the same time – and the central bank says so too – new institutional arrangements are needed to re-establish the capacity of the euro to create wealth in the eurozone, and thus a few factors of solidarity, coordination and sharing of the steering of the zone’s economy and, undoubtedly, major European projects useful for growth.

If we achieve this we shall reunite with the promise of the euro and of Europe. France has a large contribution to make. It seems to have understood this.

A speech delivered by Olivier Klein, Chief Executive Officer of the BRED Group and Professor of Economics at HEC, with Laurence Scialom, Professor of Economics at the University of Paris Nanterre, Head of the economic think tank Terra Nova, Member of the Scientific Board of the ACPR, during the third conference of the Nocturnes de l’économie, organised at the University of Paris X Nanterre by the Association Les Journées de l’Économie, on 30 March 2017.

Jean-Marc VITTORI, lead writer for the daily newspaper Les Échos

This is the third time that this exchange of views on globalisation or rather on financial deglobalisation has taken place. The world experienced a financial crisis with increases in financial trading which were extremely buoyant before 2008, and since then curves which have changed direction. What does it mean? Is it going to continue? Is it desirable? I am going to start with Olivier Klein. Olivier is a statistician and economist by training. He graduated from HEC where he teaches economics and finance. He has also been a banker for some time, and for five years, Chief Executive Officer of BRED which is the major commercial bank of the BPCE Group. BRED may well have the image of a local and regional bank, but it also has branches of the bank in South-East Asia, in the Pacific, in East Africa, and even in Switzerland, as well as a trading floor. It is thus not only a French bank. Olivier, financial globalisation, what’s the state of play?

Olivier KLEIN, Chief Executive Officer of BRED, Professor of Economics and Finance at HEC

Financial globalisation, which started around the end of the 70s, the beginning of the 80s, led to a very significant increase in international capital flows. Consequently, outstanding gross foreign assets and foreign liabilities have, for example in the United States, risen from 25% of GDP, at the beginning of the 80s – in terms of foreign assets as well as foreign liabilities, hence for assets as well as liabilities, of the United States vis-à-vis the outside world – to 150% of GDP for assets and 175% for liabilities.

With regard to France, due to the effect of the eurozone which has naturally exacerbated these phenomena, liabilities and assets vis-à-vis the rest of the world have risen from 20% at the beginning of the 80s to 300% of GDP today. The phenomenon of financial globalisation is thus very clear. From the 80s to date, the international capital market has grown beyond recognition. From 2008 until recently, a slump in GDP growth and a very strong downturn in international trade growth have been observed. It is interesting to note that this downturn did not affect international capital flows, apart from interbank liquidity flows. Interbank liquidity flows by no means reverted to the level that they had attained before the crisis.

However, with regard to the money markets, apart from the interbank markets, these flows continued to grow, even after 2008 and financial interdependence continued to increase. I will just give you an example of this, which is due, particularly after 2008, to the fact that rates in European countries and in the United State tumbled to levels that were close to zero, and occasionally even below zero, due to the financial crisis.

A carry trade phenomenon, which is well known in finance, was subsequently witnessed. As investment yields were deemed to be too low in the United States, for example, capital was borrowed in the United States and short-term investments made in emerging markets, in dollars – as the emerging markets include countries that accept the American dollar alongside their own currency – or were changed into the local currency, and in both cases were invested at higher rates than the rates that were being offered in the advanced countries of origin, the United States in this case. In so doing, they naturally encouraged growth in the emerging markets and quite rightly.

However, they also obviously created potential instability because as soon as capital leaves in search of higher short-term yields, it is also likely to flee at the slightest threat by withdrawing very quickly. This creates potential instability in emerging markets, which could be serious. This is also why in 2013, when there was a move towards limiting quantitative easing in the United States – which had facilitated the investment of enormous amounts of capital in emerging markets – the tapering announcement alone, namely the limitation of quantitative easing, sufficed to cause a sudden withdrawal of part of the capital from the emerging markets to the United States. It suddenly dried up for some emerging markets which were relying on this capital for development purposes.

This is why the Fed, the central bank of the United States, now manages its ability to raise rates or to limit quantitative easing by including this phenomenon in its calculations as it is jointly responsible for what happens in the emerging markets. However, the United States also needs the emerging markets. The Fed thus manages this in a very cautious manner, with good reason. In conclusion, the correlation between the stock markets in the United States and the stock markets in the emerging economies has risen from around 58% before 2008 to around 75% at the present time. This correlation is a consequence of this very strong financial integration. But it also displays mimicry since at some point, everything may fall or everything may rise together, which could obviously be potentially destabilising. Hence, financial globalisation has very positive effects (ability to move capital between countries with the ability to finance and countries that need finance, for example), but at the same time to potentially increase financial instability. The degree of financial instability of the system depends on the methods of regulation in place.

Jean-Marc VITTORI

This is precisely the question that I wanted to put to Laurence Scialom, Professor of Economics at the University of Paris Nanterre, a financial economics expert, a qualified member of the NGO Finance Watch, inter alia. Olivier has described this tremendous acceleration of financial globalisation in figures. He explains to us that, with the exception of one segment, namely interbank loans, this globalisation is continuing. Does it have positive effects which have often been presented as a result of these increased capital flows?

Laurence SCIALOM, Professor of Economics at the University of Paris Nanterre, Head of the economic think tank Terra Nova, Member of the Scientific Board of the ACPR

Financial globalisation was being sold to us before the crisis as providing a huge amount of benefits. It was supposed to enable better allocation of capital, better risk spreading, finance and hyper financialisation which, closely linked to financial globalisation, was meant to sustain growth. However, these promises have not been kept on the whole.

In very broad terms, the allocation of resources, international capital movements, particularly very short term ones, finance existing assets rather than real activities. They namely finance housing bubbles and stock market bubbles. This was very evident during the Asian crisis, for example. These capital inflows – notably in the emerging markets, but also in Europe before the creation of the euro – frequently had the effect of increasing the nominal exchange rate and decreasing the competitiveness of these countries. Just when it appeared to be unsustainable, there was an exchange rate crisis and capital outflows.

There are evidently problems with regard to the allocation of resources. Furthermore, the derivative markets and the risk transfer markets were sold to us as enabling better risk spreading. In fact, risk has never disappeared. Quite simply, what has in fact happened is that risk has been concentrated in relatively opaque areas. As we have seen, the crisis of 2007-2008 was the first financial engineering crisis. There had never been a crisis on this scale – the fact that a crisis created in a small segment of American finance spread throughout the world – if these products had not been packaged in securitised products which everyone had purchased as the better tranches had good ratings and did not require a capital advance, this particular crisis would not have happened.

This was a real crisis, namely a financial engineering crisis and was closely related to financial globalisation. Lastly, very recent analyses show that hyper financialisation is detrimental to growth rather than sustaining it. In fact, financial development goes hand in hand with growth up to a certain level of financial development, but all the developed countries are considerably above this level.

Conversely, financial development is detrimental to growth in all these countries. It tends to be predatory. Links have also been shown to exist between hyper financialisation and increased inequalities, namely in the analyses of Reshef, Philippon and others. None of this produced the expected results. However, paradoxically today, with the decline in interbank loans – as deglobalisation is first and foremost taking place in the banking sector and in Europe – deglobalisation is a tragedy. In fact, the resulting fragmentation of the European financial area contains the seeds of a deeper crisis, which could even lead to a euro crisis. This is actually a paradox. I believe that it is not so much a question of borders as a question of financial regulation which should be posed.

Jean-Marc VITTORI

What you are proposing to us is rather depressing because you are saying that globalisation has been disastrous and that deglobalisation is tragic… I’d like to come back to Europe because it is natural to come back there as what has happened in terms of the decline in interbank flows is largely the result of what has happened in Europe. But before coming back there, Olivier, as far as the rather critical judgement pronounced by Laurence on the effects of financial globalisation are concerned, do you share this opinion or do you think that it has nevertheless not been completely devoid of benefits?

Olivier KLEIN

I teach more or less the same thing, namely that there is quite a strong correlation between periods of financial globalisation historically and financial instability. I consequently believe that there is indeed a causal link between globalisation, when it is unregulated or poorly regulated, and the recurrence of financial crises, which have occurred time and time again since the end of the 80s, although they had ceased to exist in the developed countries during the period in which the markets were less globalised.

However, financial globalisation has also enabled, one way or another, the development of China for example. China has in fact been able to export more, by financing all or part of the current account deficit of the United States which imported its goods. It was accordingly able to base its development on exporting the goods it was producing for the developed countries. In a way and in a number of cases, with effect from the 2000s, it was because capital was circulating on the international market which countries could have used for development, not by obtaining finance from developed countries, contrary to popular belief, but by financing imports from developed countries which were coming from emerging markets. In other more classic cases, there were emerging markets that were able to accelerate their growth due to the capital that was obtained from advanced countries.

I believe that the issue is not about deciding whether globalisation is good or bad per se. That is how it should be understood, at any rate. The real issue, it seems to me, is to ask what can be done to try and limit financial instability in a financially globalised world. In that respect there are evidently a lot of questions to be asked.

When the theory is examined, it is obvious that there were some serious misconceptions inherent in the promises of financial globalisation. All things considered, it is evident that the most serious financial crises have returned. In my humble opinion, it stems from the fact that finance is inherently unstable because it is very difficult to assess a property asset by giving it a fundamental value. What is the equilibrium price of a property asset, namely an equity asset or a real estate asset? Financial markets are anticipatory.

Whenever an asset is bought or sold it is because there is an anticipation of the future trend in the price of this asset in one direction or another. These markets are sensitive to shifts in sentiment, hence to mimicry, to conventions, because the future is de facto difficult to predict as the asymmetry of information on financial assets is significant and because, as a result, the cognitive biases of the players are decisive.

However, this does not mean that financial markets are not needed as well as banks. Not only are banks necessary, financial markets are as well. Banks cannot do everything, firstly, because they have amounts of capital assets that are necessarily limited for the purpose of making loans, while observing their own solvency ratios and secondly, because financing requirements are far greater than the financing capabilities of banks.

Banks are indispensable and are the economic factors that most frequently provide stabilising effects because they are regulated and manage long-term relationships with their customers, with the aim of ensuring that they repay the loans granted and do not play on the variation in the instantaneous valuation of their commitments based on very short-term market developments. They are accordingly much less sensitive to sudden shifts in sentiment that are inherent in financial markets, which do not set a benchmark for the fundamental value shown.

However, financial markets concomitantly provide additional support to the action taken by banks in terms of financing the economy, as I have just said, as well as their ability to spread exchange rate, interest rate, credit risks, etc., as a result of the derivative markets. It should be emphasised that the division of the share of funding borne by the financial markets and the share borne by the banks is also a structural issue which partially determines the overall level of financial stability.

Lastly, it is all very well to regulate the banks themselves, but it is by no means sufficient. Moreover, at this moment we are seeing that investment funds, investment trusts, insurers, all of shadow banking generally, are starting to take risks for which they are not regulated and for which they do not always have proven expertise. In my opinion, that could present a problem in the coming years, particularly during the next real economic crisis or even during a sharp downturn. Regulation must apply to all players, otherwise it is inadequate by definition and encourages circumvention of the regulations.

Yes, of course, there is inherent financial instability. And yes, there is a need for finance. This means finding the theoretical and practical means that would enable it to be regulated as well as possible to prevent systemic crises.

Jean-Marc VITTORI

So finance is necessary. This finance is inherently unstable so it must be regulated, all the more as globalisation is continuing. What are the main sectors which require action?

Laurence SCIALOM

I think that we are now at a crossroads. We have made progress in certain areas. Banks are undeniably better capitalised but, at the same time, they had previously been so badly capitalised that even if they had tripled their capital, it would not have sufficed. I also think that there is a false sense of security, in other words to prevent the banks from capitalising further, they are compelled to issue types of debt that enable a bail-in. In other words, to avoid asking the taxpayer, a decision was made to ask those individuals and entities that have claims against the banks. These are the famous bail-in instruments.

The problem is that I am firmly convinced that this is not feasible in the event of a systemic crisis because it is likely to create mass contagion, as we have seen. In Italy, which was nevertheless a rather specific case as savers were holding securities, but the taxpayer was obviously on the front line there. But in the event of a systemic crisis, I think that it would be a vehicle for propagation purposes. Because who holds them? They are different financial players…

Enormous progress has been made in enacting bank liquidity regulations. However imperfect they are, they recognise that liquidity risk is the Achilles’ heel of banks, and particularly of European banks due to their funding structure, which is very dependent on obtaining liquidity on wholesale funding markets. In my opinion, insufficient progress has been made in regulating shadow banking. This time, the action that has been taken falls far short of the action that should have been taken. A particularly serious issue is the excessively close ties between systemic banks and shadow banking. Interbank loans have declined, but not loans by banks to shadow banking. This is patently obvious in the latest empirical analyses of these issues.

I also think that the issue of banks that were “too big to fail” has not been properly addressed. Following on from what I have said about the bail-in, I am convinced that the implicit Government guarantees will continue to have enormous consequences for all banks. This is why I personally was in favour – and am still in favour – of a separation… but not along the lines of the Glass-Steagall Act, but rather a separation along the lines of Vickers and Liikanen, in other words subsidiary creation, with different capital ratios, different boards of directors, etc.

Jean-Marc VITTORI

Before giving the floor to the students for their questions, I would nevertheless like to talk about the specific situation in Europe. Something has clearly happened in Europe with regard to financial globalisation which has undergone a major departure from financial globalisation. Olivier, how do you explain this? How is it going to develop?

Olivier KLEIN

Europe is in fact the one place in the world which is witnessing financial deglobalisation, and this is not good news at all. My interpretation is simple. The eurozone is unfinished. I myself was in favour of the eurozone, I simply said that in order for it function efficiently and sustainably it required elements which are more than the sum total of convergence criteria. As in the US dollar zone in the United States, there no coordination of economic policies and possibilities of making either fiscal transfers or partial debt mutualisation, which ultimately also involves fiscal transfers. This has not been done.

And the markets did not notice. From the creation of the euro until 2010, they have failed to pose the right questions. Then they suddenly realised that contrary to what they had imagined – they had believed that they could look at the current account balances across the eurozone, and not for each country, that there were countries with large current account deficits which could have found it difficult to obtain funding without the solidarity mechanism within the eurozone. The markets took fright and suddenly, quite naturally, triggered a brutal, contagious and dangerous cycle of national public debt and interest rates, embroiling these countries in a vicious circle which could have triggered the collapse of the eurozone. No one was willing any more to provide funding to those countries in the eurozone with a large current account deficit. Fortunately, Mario Draghi intervened and explained that the CEB was going to protect the eurozone by purchasing public debt, then by implementing quantitative easing and last but not least by stating the famous “whatever it takes” in 2012.

Without that, the eurozone would have collapsed. Today, the fact is that the eurozone still does not have a private equity market which finances, through the surpluses of countries with a surplus, countries with a current account deficit. It goes through the euro system, through the European Central Bank. This becomes evident, by taking a closer look at the situation, in the Target 2 balances. Countries with a current account surplus are lending more and more to the central bank and countries with a deficit are borrowing more and more from the same central bank. This represents the cumulated current account positions and financial positions of these countries.

This is the way countries with a current account deficit are obtaining funding for the time being, de facto without the assistance of the markets. This is naturally not sustainable as there may be countries – and Germany is one – that sooner or later are likely to refuse to structurally fund countries with continually growing deficits via the euro system, while they themselves have growing surpluses. Even if these surpluses and these deficits are also the result of the structural setup of the eurozone as it exists today, they are nevertheless unsustainable.

We now have a situation in the eurozone where the private equity market no longer functions. Everything relies on the central banking system, namely the euro system. To enable the system to work well and for the markets to accordingly resume their role, we lack the degree of trust that is required between the countries in the eurozone and the cultural bond that could result in solidarity, even partial, between them. This would manifest in several aspects of federalism and would lead to full monetary union and hence a more stable monetary zone.

In this regard, the fact that France is implementing its essential structural reforms is the condition that is essential to enable Germany to envisage the implementation of elements of solidarity in the system.

Jean-Marc VITTORI

Laurence, I think that you have outlined the main points.

Laurence SCIALOM

Financial fragmentation in Europe today is a result of the fact that the euro is an incomplete currency. The aims of the central currency have been federalised but the fact that over 80 % of the currency that is created is banking currency has been forgotten. Moreover, Europe has banking systems that are excessively concentrated with very large banks. Of course, when the situation started becoming rather critical, the banking union was created.

What is the banking union? It means that the largest systemic banks are going to be supervised at federal level and that the problems are also going to be resolved at federal level. However, there is a third pillar which remains unresolved, namely federal deposit insurance. As long as this third pillar has not been constructed, as long as we are not out of the woods, one euro in a Greek bank will not be worth one in a German bank, for the simple reason that the Greek depositor is less well protected than the German depositor. This was very evident when the situation with regard to Italian banks became strained. You have a great deal of Italian bank assets that had been invested with banks in countries that appeared to be more robust.

As long as there is no back-stop, namely a dose of federalism, as has just been mentioned, and as long as Member States are called upon to bail in their own banks, we are not out of the woods.

To re-establish sustainable growth, investing in people now appears to be imperative. Three major economic developments lead me to this conviction.

The innovation economy places knowledge at the heart of competitiveness

The first, as stated by Philippe Aghion in his excellent work on growth theory, is that we are no longer in a catch-up economy, as was the case after World War II. An economy in which we needed to re-establish demand levels, standards of living and, more generally, to catch up on those countries not affected by the war in the same way as us and therefore lagging behind much less.

In the 1980s our economy entered an innovation phase. Growth is clearly still a function of the dynamics of demand but, today, it is at least as much dependent on those of supply. The dynamics of supply are a direct result of innovation and R&D capacity. These are the decisive growth factors in the modern world. Technical progress, creative capacity and the creation and development of new technologies, and even the creation of new markets, are of critical importance.

This being the case, new growth will only be attained through significant investment in human capital.

The search for added value requires higher qualifications

The second point I would like to discuss links into and concludes the first: globalisation. The emerging countries are progressing and rapidly catching up on the developed world. They have no other choice but to innovate if they wish to remain on the path of high growth.

Put simply, faced with globalisation, developed economies can adopt two different differentiation models.

Firstly, an economy with a medium level of added value, producing mid-range products, which demands low levels of labour costs and social benefits in order to remain competitive with the emerging economies.

Secondly, a route which can justify the retention of high salaries and benefits, by seeking out high added value through high-end market positioning. We’re not talking about luxury here, but of production located on the high side of the technology curve generating higher added value, which can only be attained through reforms that encourage research and development alongside significant investment in human capital.

And we have two such characteristic examples in the eurozone. On the one side there is Germany, which has enjoyed a globally satisfactory growth rate with low unemployment, a very high current account surplus and zero budget deficit. On the other side we have Spain, which has been forced to reduce labour costs to “pull through” as its output lies in the middle of the range. For all that, its major efforts have borne fruit in economic terms, but have had the all-too-familiar socio-political effects.

For its part, France lies somewhere in the middle. In reality, its added value is somewhat average and has not reformed sufficiently to move up-range, or made much effort in the area of labour costs. It therefore has an unemployment rate twice that of Germany, lower average growth and high public and current account deficits.

The search for high added value production unavoidably calls for positioning at the frontier of technology, which requires investment in training, education and, more generally, in human capital.

In this light, it is important to stress that France has not been on the right path in this regard for some fifteen years. If we take the PISA comparisons from the OECD, which measure educational attainment at the age of fifteen in writing, maths, sciences and problem solving, France, which was already only in 13th place in 2000 with 511 within the OECD, was 25th in 2012 with 495 points. It has both fewer points and a lower ranking. This says nothing for the fact that over 20% of 11-year-olds are unable to master the basic skills.

The second OECD study, the PIAAC, places competence levels of French workers vis-à-vis company requirements in just 22nd place within the OECD.

Organisational structure and management generating higher company resilience and greater employee autonomy

The third main reason, both economic and entrepreneurial, is the introduction of digital. The digital revolution facing us not only changes customer behaviour, but clearly also that of employees.

The management and organisation of today’s company has fundamentally changed. A high performing company must now meet a growing demand for autonomy expressed on a daily basis just as much by the customer as by the employee. These developments call for a world that is much more horizontal than vertical. Employees need to understand, participate and feel more involved with less strict hierarchies. We must therefore expand collaborative working environments and give more meaning to the work of the individual.

And this is why management itself must change. Managers can no longer base their legitimacy on the control of access to information but on their ability to lead their teams, by positioning themselves in front of them and not behind, happy simply to supervise. They must provide direction by explaining and involving, such that employees feel fully motivated and committed.

Here, the clear objective is to have an attractive company with loyal employees fully signed up to the corporate mission. But it is at least as important to promote a competitive model, as this offers greater autonomy to employees and all other parties. This increased autonomy is essential if companies are to maintain flexibility in the face of all the challenges of the modern world, capable of adapting quickly and easily to ensure continued survival. Structures organised more into networks, leaving greater autonomy to their constituent parts, closer to both the customer and employees, are less rigid, less fragile. Conversely, vertical and more centralised hierarchies are less able to confront rapid and continuous change. So by introducing greater autonomy into the system – clearly while maintaining overall cohesion – companies are capable of absorbing exterior shocks, becoming more responsive, more agile and globally more resilient.

In this context, investing in human capital is vital in order to anchor the individual’s capacity to exert their autonomy. It requires continuous investment in training. It cannot be imposed from above.

Counting on intelligence to “come out on top”

Fundamentally, confronting incessant competitive change means relying on intelligence. To be an innovator, a creator and not a follower, at both the company and national level, to be competitive, to find solutions to “come out on top” in the crises we know all too well, to seek out added value, to be effective, to motivate employees, to be able to tackle incessant change – all of these challenges require investment in human capital.

In all modesty, we are continually seeking to “come out on top” at BRED. The banks are going through a very difficult period confronting the threat to their revenues, notably due to interest rate developments and over-regulation. We are seeking to offer our customers higher added value. This path requires investment in our men and women. And this is precisely what we are doing by making significant investment in digitalisation, by improving our tools and services for our customers and employees, but also by investing heavily in our staff to ensure that they are fully able to understand, share and co-construct the strategy and corresponding organisational structure at every level. In partnership with HEC, we have also created an internal management school at BRED which is working remarkably well, where we notably push managers to reflect on the very nature of the role of manager in the world of today and tomorrow.