Stablecoins are experiencing explosive growth as a means of settlement. In 2024, they processed more transactions than Visa and Mastercard combined. Unlike “pure” cryptocurrencies, which are issued without any backing and whose value is inherently speculative and highly volatile-since it depends solely on the self-referential opinion of the market-stablecoins are cryptocurrencies backed by assets such as the dollar. For each unit of stablecoin issued and purchased in exchange of any currency, the amount received is immediately used to buy U.S. dollars and invested in U.S. Treasury securities. It is this one-to-one rule that makes these specific cryptocurrencies “stable” rather than purely speculative.

Amid rising uncertainties in the U.S. bond market, reflected by a reduction in Treasury purchases, the United States sees stablecoins as a strategic opportunity: to attract new demand for its sovereign debt and reinforce the dollar’s dominance in global trade. Indeed, the more dollar-backed stablecoins are used internationally, the more issuers must acquire U.S. debt to guarantee their value. Washington thus could use stablecoins as a tool to refinance its external debt while expanding the dollarization of the global economy. The recent adoption of the Genius Act bill, supported by the U.S. administration, aims to support and regulate the development of dollar-backed stablecoins, giving American issuers a competitive advantage and consolidating the dollar’s supremacy.

This strategy is not without risk for the rest of the world. The possible massive adoption of dollar-backed stablecoins could accelerate capital flight from emerging or fragile economies, as citizens seek protection from inflation or currency devaluation by turning to these stable payment methods. More broadly, stablecoins weaken the monetary sovereignty of countries outside the United States, reduce their ability to finance their economies with local savings, and expose their financial systems to risks of banking disintermediation. The global reallocation of savings toward stablecoins backed by U.S. debt diverts resources from local private sector financing to the benefit of the U.S. Treasury. National banks, deprived of deposits, see their lending capacity shrink accordingly, slowing economic growth in these countries.

Finally, the expansion of stablecoins poses major challenges in terms of regulation, anti-money laundering efforts, and consumer protection. These assets can circulate without constraint, facilitating illicit flows and eroding the integrity of financial markets.

Ultimately, increased dependence on the dollar via stablecoins further entrenches the asymmetry of the international monetary system, making economies-especially emerging ones-even more vulnerable to U.S. monetary policy decisions. In sum, by developing dollar-backed stablecoins, the United States has gained an unprecedented lever to further dollarize global trade and refinance its external debt. But this strategy imposes significant risks on the monetary sovereignty, financial stability, and economic development of the rest of the world.

But it’s a double-edged sword for the United States. Stablecoins can also accelerate both the appreciation and depreciation of the dollar, thereby increasing macro-financial volatility.

Olivier Klein Professor of Economics at HEC and Banker

Published by Les Échos on April 7, modified and completed on April 10

Trump has a few central economic ideas that seem to guide his words and actions. And while he appears to many to be disorderly, incoherent, and contradictory, his worries are not devoid of both a sense of reality and coherence. But he seems to have only one weapon to achieve his goals, wielded in a brutal and crude manner: tariffs. Doubtless, along with a weakening of the dollar. But the wielding of these weapons is contradictory and dangerous.

The difficulties of the American economy are not due to its growth rate or productivity gains, which have been significantly higher than those of the Eurozone, particularly for the past fifteen years. On the other hand, between 2000 and 2024, the share of industry in GDP fell from 23% to 17%, with the resulting adverse effects on American workers and middle class.

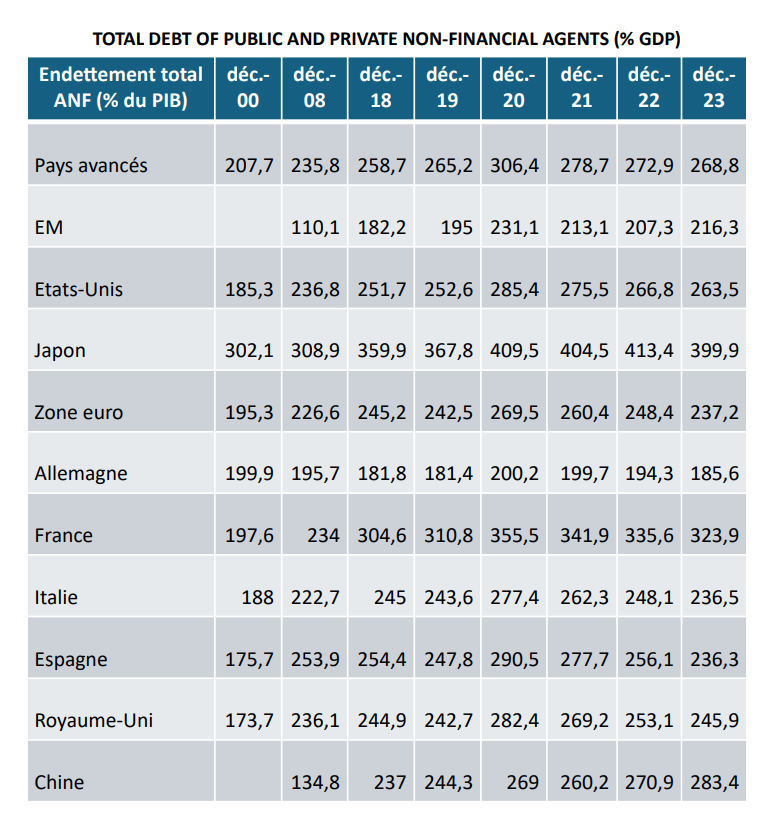

Furthermore, the twin deficits, public and current, have led, over the last twenty-five years, the United States to see its public debt soar from 54% to 122% of GDP and its net external debt multiplied by a factor of 4 (approximately from 20% to 80% of GDP).

Monetary Dilemma

This explosion of both debts will sooner or later pose a problem regarding the dollar’s status as an international currency. However, the United States has a structural need to finance its debts, and therefore a need to attract capital from the rest of the world. And owning the international currency (approximately 90% of foreign exchange transactions, 45% of international transaction payments, 60% of official central bank reserves) greatly facilitates this financing, since countries with a current account surplus, most often in dollars, almost systematically reinvest this liquidity in the American financial market. Especially since the United States has outperforming equity returns, and by far the deepest capital market.

This status as an international currency also requires the country with this considerable advantage to accumulate a current account deficit over the years so that the rest of the world can hold the amount of international currency it needs, quasi automatically financing this deficit.

But, as in all things, balance is essential, and in this matter, it is difficult to maintain. The United States does not regulate the size of its deficits and debts according to the needs of the rest of the world, but according to its own needs. This, moreover, gives the international monetary system an intrinsically unstable character, as the global currency is merely the debt of one of the system’s players imposed on the others, and not that of an ad hoc institution, not being one of the players themselves.

Robert Triffin, as early as the 1960s, stated that if the United States did not run a sufficient current account deficit, the system would perish from asphyxia. And if this deficit (and therefore the external debt) became too large, the system would die from a lack of confidence.

Faced with the dangerous dynamics of external debt in particular, today Trump must therefore protect confidence in the dollar to perpetuate its financing by the rest of the world without (too much) pain, that is to say at non-prohibitive rates, and, at the same time, try to reduce excess imports compared to exports so that the trajectory of this debt can be sustainable. With a coherent objective of reindustrialisation, thus making it possible to reduce this gap, by limiting imports of industrial products, while making his voters happy.

So Trump is right to be concerned about the unsustainable trajectory of U.S. external debt. The dollar’s role as an international currency goes hand in hand with current account deficits for the country issuing such a currency. However, if these deficits become too large and external debt grows excessively relative to GDP, U.S. creditors might lose confidence in the dollar, potentially causing its value to drop significantly and/or increasing refinancing rates due to higher risk premiums demanded by the global market. This concern is justified.

Fragile Confidence in the Dollar

Yet, Trump seems to have only one weapon in his arsenal to achieve this: tariffs. And the apparent aim of weakening the dollar. At first glance, indeed, both an increase in tariffs and a weakening of the dollar can simultaneously lead to a decline in US imports, an increase in domestic production and in exports, and a need for non-Americans to develop their industries within the United States to maintain their commercial presence.

However, this strategy, while seemingly coherent, clashes with the contradictory need for a stable dollar if we wish to maintain the confidence of the rest of the world, which buys US debt.

Furthermore, the weaponisation of the dollar by previous administrations to enforce financial sanctions imposed by the United States, has already seriously damaged the confidence and desire of the rest of the world to hold unlimited amounts of dollars. Those of the “Global South” countries in particular, which are simultaneously challenging the American double standard.

In addition, the abrupt and seemingly erratic announcements regarding huge tariffs increases are also not fostering confidence in the American economic and financial system, to say the least. This is without even considering their very dangerously regressive potential for the global economy.

Let us also incidentally note that Biden’s IRA had effects similar to tariffs – though much less abruptly and violently- by heavily subsidizing industries producing exclusively in the U.S., which violates WTO rules.

Additionally, the Trump’s idea that the imbalance between U.S. imports and exports is primarily due to unfavorable and unfair conditions imposed by surplus countries is incorrect. While China has built its growth on exports while restricting access to its market, the significant U.S. current account deficit mainly stems from an insufficient domestic competitiveness and from a strong lack of savings compared to investment, that is to say from demand being much greater than domestic supply, leading to huge current deficits and consequently to a evergrowing reliance on external financing.

Instead, structural measures to enhance U.S. industrial competitiveness and public deficit reduction are essential. In summary, while concerns about maintaining a sustainable trajectory for U.S. external debt are justified, balancing individual current accounts with each country based on perceived abuses by surplus nations is totally misguiding. Furthermore, aggressive use of tariffs or dollar manipulation reflects a crude and dangerous approach to economic policy that is risky, even as a negotiation tool. And lacks theoretical as well as empirical legitimacy.

Protecting Financial Stability

Trump is therefore right about his “obsessions,” but undoubtedly wrong in the nature of his response.

He also brandishes threats against countries that are considering creating alternative payment systems to the dollar, and perhaps soon against those that channel less of their excess savings into American financial markets.

And perhaps he also dreams of transforming their debt obligations to the United States into very long-term, low-interest debt (see Stephen Miran, Chairman of Trump’s Council of Economic Advisers). This would, of course, definitely precipitate the rest of the world’s loss of confidence in the dollar.

It is also possible, with the same objective, that he is considering facilitating the development of stablecoins, cryptocurrencies backed by the dollar, in the hope that they will spread worldwide, thus de facto dollarizing the planet. To the detriment of the monetary sovereignty of other regions of the world. We can therefore bet that, in countries around the world, authorities would prevent this by regulating payments within their borders, thus protecting their sovereignty and global monetary and financial stability.

The economic and financial challenges facing the United States are significant. But the solutions to address them are certainly more diverse and more structural than simply imposing tarifs. And, much worse still, very high tariffs, with inevitable retaliatory measures, would lead to a huge global recession combined with a major financial crash.

We are at a real turning point in the history of Europe. In this changing world, which has turned its back on multilateralism and today faces the pure and simple return to the balance of power between nations, one of two things will happen: either Europe pulls itself together economically, politically, diplomatically and militarily, or Europe that is half-asleep continues its decline and gradually disappears from history.

But getting its act together will not be easy. If Europe has clean hands today, it is heading towards having no hands at all. Let us put an end to our inability to be bold and innovative on our aging continent, due to the constant desire to regulate and standardise before inventing, creating and developing. Furthermore, to force the rest of the world to follow our standards is naive; we have neither the economic nor the diplomatic power to impose them on others.

Let us stop thinking of ourselves in Europe as the camp of the self-righteous, by developing for ourselves at every turn finicky regulations where the letter ends up prevailing over the spirit. They end up hindering our companies, with endless bureaucracy. These are worthwhile goals, but the never-ending red tape needlessly damages our competitiveness.

Let us do away with our naivety in wanting to be continuously top of the class on climate, when this leads directly to the detriment of our industries and de facto favours populism which has a strong climate skepticism. Let us instead seek to best combine the health of the planet and growth, by investing massively in the industries of the future – where we have no presence – including in the climate transition industries – where we are so weak.

Let us also leave behind our naivety when it comes to energy, where yesterday we were subjugated to Russia, and tomorrow to the United States. It is essential for our global competitiveness. Currently we are on average paying at least five times more than the Americans for the price of natural gas.

Let us think that the single financial market would be highly desirable, but that it would not produce the expected effect on its own. The surplus of European savings will spontaneously finance more investments in Europe – only if we establish an explicit framework of financial solidarity within the euro zone. For this, the public finances of France, among other countries, must finally be credible. Risk sharing versus market discipline, right? We also need a European capacity to facilitate the development of our newly created companies to make them global giants. And thus provide attractive returns.

The multiple non-financial barriers to doing so are crippling.

Europe no longer knows how to correctly combine the principle of ethics and that of efficiency. Ethics alone, constructed as an absolute end, to the detriment of efficiency, is only a short lived illusion that we create for ourselves. The reverse is also true. But today, multifaceted, quasi-dogmatic formal ethics has ideologically taken too much precedence over its indispensable partner and unduly hinders it. It is the right balance between regulation and free play of the market that we must aim for. One that enables the dynamics of the economy while seeking the necessary protection against its potential excesses.

Europe has been, and can once again become, the place on earth that best combines these two principles. This has made our social market economy model so strong. It is up to pro-European democratic forces to vigorously regain the vitality and balance they need. Before others impose a brutal paradigm shift on us.

It is only through this renewed vitality that Europe will be able to continue to chart its course and control its destiny. This is an urgent matter.

To fully understand this, it seems necessary to make a clear distinction between the quantitative easing policy of central banks consisting of massively supplying banks and markets with “liquidity”, to be more precise in the money of issuing institutions, prolonging and broadening their historical action of last resort, and that consisting of the purchase of assets on the financial markets, public and private bonds, or even stocks. These two ways of conducting a QE policy induce the same inflation of the assets and liabilities of central banks, but by different means. In the first case the monetary authorities lend to banks, in very unusual circumstances, in order to avoid a liquidity shortage in the banking system. In the second, in equally unusual circumstances they buy assets from non-banking agents who, by selling them to central banks, receive money that they deposit in the banks; the latter thus ultimately holding more central bank money in their accounts with issuing institutions. We could call the first a policy of the liabilities of the balance sheet of central banks and the second an asset policy.

But the most fundamental distinction lies in the circumstances leading to the use of these policies. In the United States, as in Europe for example, they were initially used to deal with the very serious financial and economic crisis of 2008-2009. The risk of a chain of bank failures, as well as market dislocation, required breaking these catastrophic dynamics by temporarily suspending the logic of the financial markets and the contagious distrust between the banks themselves. Which could also have led to a destructive crisis of confidence among households in their own banks. Thus, the central banks increased their balance sheets to provide the banks with the necessary liquidity. De facto, with the interbank market frozen, they interposed their balance sheets even in the exchanges of liquidity between banks. Banks with excess liquidity no longer lent to other banks and kept their central bank money in deposits at the central bank, with the issuing institution itself then lending to banks requiring liquidity. This operation of credit thus adds liquidity in the banking system and inflates the Central Bank’s balance sheet. This is how central banks were once again the lenders of last resort to the financial system from 2008. But it was also in 2008 that the Fed decided to buy “toxic” assets to prevent the loss of confidence and bankruptcy of those who held them. And also to prevent the collapse of the price of these assets, the consequences of which would have been potentially disastrous for the economy. This is how central banks were able to curb the systemic risk that was developing

very quickly and which would otherwise have led to catastrophic economic and social consequences. The same was true around March 2020, during the very severe financial flash crisis due to COVID and lockdowns. Central banks then bought many assets, including high yield assets, particularly from non-banking financial institutions, including troubled investment funds, which made it possible to very quickly extinguish the fire that was suddenly taking hold.

Quantitative easing was then used and perpetuated with a completely different objective. The violent financial crisis was over, and as a result, the economy was very slow and inflation was at extremely low levels. With interest rates close to their effective lower bound, the weapon of key interest rates in conventional policy had become ineffective. This is why central banks began to buy financial assets to stimulate the economy and try to raise inflation. Then in 2020, with the economic consequences of the pandemic and lockdowns, they did the same. They have notably bought public debt bonds, in order to support the government’s very important fiscal efforts.

The effectiveness of this policy may come from the very announcement of the implementation of such a decision. The OMT program, for example, announced in 2012, led to a rebound in confidence following its presentation, even though it was never implemented. But its effectiveness may also come, of course, from the possibility it offers central banks to take control of long-term interest rates and risk premiums, or at least to substantially influence them. In this way, they can encourage households and businesses to invest, or even consume, more, in particular by lowering the cost of their loans. Credit, and its twin, debt, have also gradually recovered since around 2017 in Europe. The third transmission channel was the wealth effect triggered as a result of the fall in long-term rates on the value of stocks as well as on real estate. This wealth effect has thus supported demand.

Let us stress, however, that such a policy of quantitative easing outside of a situation of financial stress, to be effective, that is to say to stimulate the economy, must require central banks to buy much more assets, that is to say to create much more central bank money, than during financial crises. However, even if it requires injecting even more liquidity to reinvigorate economic growth as well as credit growth, this policy of purchasing assets has been useful. It has notably prevented a triggering of a deflationist cycle.

However, it failed to raise inflation. It is likely that the 2% inflation target did not correspond to a rate that met the contemporary mode of economic regulation, that is, the prevailing structural conditions during the pre-COVID period. The combination of a sustained situation of globalisation, which weighed on wages and prices in developed countries, and a technological revolution that gave little room for manoeuvre in wage negotiations for low- and medium-skilled employees, helped by digitalisation and robotisation, induced the structural causes of very low inflation, perhaps around 1%. The efforts of central banks, seeking to stimulate the economy and inflation, then succeeded in increasing the growth rate, but not the level of inflation. And, in its search for an inflation target that is probably unattainable as well as with the help of a compass – the natural interest rate – that is very imprecise and conceptually questionable, monetary policy has persisted in using quantitative easing, even though GDP and credits had returned to a favorable trend. The consequence has been interest rates that have been too low for too long, that is to say, sustainably lower than growth rates. With, as a result, the rise of financial instability due to a strong growth in the indebtedness of private and public agents (in relation to GDP) and in a feedback loop with this increase in indebtedness and the very rapid and very strong rise in the value of stocks and real estate. Indeed, with long-term interest rates lower than the nominal growth rate, private and public players were encouraged to painlessly increase their debts, thus weakening their balance sheet.

And savers, or their asset managers, their pension funds or savings funds, like their life insurers, have sought to obtain a sufficient return. They have thus been encouraged to buy increasingly risky assets (drastically lowering risk premiums), increasingly long-term assets (thus taking on more and more liquidity risks), etc. The balance sheets of many economic players have thus become fragile both on the assets and liabilities side.

Furthermore, very accommodative monetary policies that persist for too long de facto increase wealth inequalities, further enriching those who already have some, and making real estate and the stock market less accessible to others. Finally, with all these effects combined, it is reasonable to think that they have ultimately contributed to the slowdown, to the languishing of the economy, by having notably allowed the development of “zombie” companies (which, with normal interest rates, would have experienced negative results).

This overall poor allocation of capital has very probably contributed to decreasing productivity gains. Furthermore, interest rates that are too low for too long may have, as in Germany for example, contributed to the rise in savings rates and not to their decline, contrary to the precepts of standard economic theory. A population with a declining demographic may indeed want to save more to prepare for its retirement, no longer being able to count sufficiently on the return on its “normal” savings. The high level of indebtedness of many players also sooner or later weighs on their investment capacity. All of these factors then lead to a structural slowdown in growth and not its support .

To conclude, it is difficult to exit quantitative easing policies once they have been used for too long. Thus the policies have developed asymmetrical characteristics which could be worrying. Among other things, this asymmetry can provide markets with free options to protect them on the downside while allowing them to play the upside with very limited risk. The consequent fragility accentuated in the financial structures of agents, both in the assets of balance sheets, which include highly valued or overval ued stocks and real estate, and in their liabilities, which have levels of debt to GDP rarely reached, rightly enco urages central banks to be very cautious in their balance sheet reduction (“quantitative tightening”). Reducing the balance sheet of issuing institutions too quickly or too intensely could indeed lead to major financial and economic crises. This is why we can consider that liquidity in central bank money will only be withdrawn – as at present – very cautiously. In fact, very probably, the opposite path will never fully reach its end. Furtherm ore, we are in an unprecedented realm since the experience of “quantitative tightening” is a historical first. The fight against the sudden return of inflation these last years has been successful thanks to conventional monetary policy effects (raising their pol icy rates) , without acting discretionarily on their balance sheet size, but driving their l ow-key reduction.

Ultimately, it seems that we can affirm, based on a retrospective analysis, that quantitative easing policies have very favorable effects when it comes to healing a violent financial and economic crisis by trying to contain systemic risk, that is to say, to prevent a catastrophic chain of events. However, if it is also useful to use them to stimulate growth and inflation, if we continue to use them, even when growth has returned, and, moreover, if the target inflation no longer corresponds to structural inflation, this may seem to entail more dangers than benefits. We have not yet seen all the economic and financial consequences that such a policy pursued for too long can induce. Let us bet that, barring new violent crises, and across cycles, central banks will seek to sustainably maintain interest rates at levels roughly equal to nominal growth rates. All things considered, and in order to be able to use it again in case of proven need, the unconventional monetary policy should remain unconventional.

Olivier Klein Chief Executive Officer Lazard Frères Banque Professor of Economics and Finance at HEC

BIBLIOGRAPHY

Exiting the ECB’s highly accommodating monetary policy : stakes and challenges – Le Blog Note d’Olivier Klein Revue d’Economie Financière – https://www.oklein.fr/en/exiting-the-ecbs-highly-accomodating-monetary-policy-stakes- and-challenges-2/

HOW CAN WE AVOID THE DEBT TRAP AFTER THE PANDEMIC? – Le Blog Note d’Olivier

KLEIN Revue d’Economie Financière – https://www.oklein.fr/en/how-can-we-avoid-the-debt-trap-after-the-pandemic/

The benefits and costs of asset purchases ECB – https://www.ecb.europa.eu/press/key/date/2024/html/ ecb.sp240528~a4f151497d.en.html

After having surprised us with its vigour, inflation, due to a demand shock – which rebounded very strongly once the lockdowns ended – and to a supply shock – dramatically reduced during the pandemic -, seems to be gradually returning to acceptable levels. The causes of this decline can be attributed to a gradual increase in global production capacities and the fall in excess demand through the deflation of excess savings generated by the lockdowns. But disinflation was also caused by a very reactive and internationally coordinated monetary policy as well as the strong credibility of central banks who showed great determination in wanting to bring inflation back on target. This has ensured that the inflation expectations of the various economic actors – businesses and households – do not become dislodged. Let us add that until now, contrary to a number of forecasts based on historical data, we have witnessed a soft landing of the economy, that is to say without recession and without any systemic financial shock. So is the game won? Quite possibly. However, several points should make us cautious about this diagnosis.

Salaries have recently increased at a rate that remains high (between 4 and 5% per year). However, in the euro zone, almost zero productivity gains make it impossible to compensate for this increase. Corporate margins are therefore at stake. Continuing in the euro zone, it is the fall in import prices which has provided a large portion of the disinflation. But can they continue to fall further? And prices for services continue to rise rapidly. Furthermore, until now, the sharp increase in interest rates in a context of historically very high public and private debts has not produced the financial impact that was feared. And yet hadn’t we talked about a possible “perfect storm” on this topic? Some reasons for this non-event: increased savings and inflation protection policies have fuelled growth which helps overcome rising costs of debt. Banking regulations, significantly tightened since the last major financial crisis (2007-2009), have generally succeeded in safeguarding the banks.

Companies, taking advantage of the very low rates preceding the return of inflation, had extended their loans and had taken them out at a fixed rate instead. However, let’s keep in mind a few elements that also encourage caution. The professional real estate sector, during the real estate bubble preceding the pandemic, may have experienced excess debt here and there, resulting in insolvencies beginning to appear. Many companies in all sectors, sometimes with high leverage, will have to refinance their loans over the next few years. States themselves, which are highly indebted, will gradually have to bear sharply increasing interest charges which will disrupt their solvency trajectories. The sensitivity of financial markets to this type of situation could thus increase significantly. In addition, central banks will certainly be keen not to reproduce periods of interest rates that are too low for too long, periods which weaken financial stability. And they will want to maintain room for manoeuvre to deal with future systemic crises. Inflation, moreover, for structural reasons, will no longer be as low as during the last 30 years.

We should therefore have changed our interest rate regime a long time ago, returning to more normal rates, that is to say closer to nominal growth rates. Also, if the situation so far has proven to be a successful landing of inflation without major damage to the economy, to avoid a large-scale upheaval that is still possible, it is therefore up to private and public economic actors, supported by macro-prudential rules well established by the concerned authorities, to adapt vigorously to ensure the sustainability of their solvency and their growth.

The concept of structural reforms is not well understood. Their purpose is, in fact, to boost a country’s economic growth potential, without necessarily lowering wages or social protection through austerity measures. It is important to clarify this distinction, as confusion can be detrimental to the discussion.

Why is it essential to increase France’s growth potential? Firstly, to lower the structural unemployment rate, which, despite recent progress, is still around 7 percent. The country also faces unacceptably high youth unemployment, at around 18 percent (compared to 5 percent in Germany). Secondly, increasing growth potential would help ensure a better financial position for the state, local authorities, and social security, which would lead to increased sustainability for social protection and pensions. There is no point in dissociating the financial question from the capacity to maintain a high level of social welfare.

Thirdly, France needs to seek competitiveness from above, which can be achieved through two possibilities: lowering the cost of labor and social protection via austerity policies – as was the case in Spain and Portugal during their debt crisis and the financing of their foreign trade deficit, during the euro zone crisis of the 2010s. Or, on the other hand, improving quality-price ratios of national products and services through structural reforms, such as developing added value and the range of production, notably through innovation. Public expenditure must also be managed efficiently to avoid excessively high tax rates, which could reduce competitiveness and employment and jeopardize the sustainability of social welfare.

Germany has been successful in this regard since 2000, with reforms that have strengthened its competitiveness despite having one of the highest labor costs in Europe, through industrialization based on high added value. This resulted in a high trade surplus, a structurally low unemployment rate, and a relatively low public debt ratio.

France has a similar labor cost to Germany but needs to improve its production range and quality-price ratio, as it currently offers a low quality-price ratio. As a result, the country has a low level of industrialization and a trade deficit that is constantly deteriorating. France’s lack of structural reforms over the past few decades has led to an excessively high unemployment rate, one of the lowest employment rates among comparable countries (68 percent compared to 77 percent in Germany and Sweden or 82 percent in the Netherlands), and a high permanent budget deficit, resulting in an excessive and steadily rising level of public debt.

The potential growth rate of an economy is the sum of the growth rate of the working population and productivity gains. France needs to implement several structural reforms to increase the quantity of work, which is one of the lowest in relation to its population (610 hours of work per year and per inhabitant, compared to more than 700 in Germany or 750 to 900 in the Netherlands, Sweden or Portugal). This would help finance social protection for all and public services, so their level does not fall. A better functioning labor market is essential to achieve this, which would also put an end to the paradox of a still too high unemployment rate coexisting with a high proportion of companies unable to recruit as much as they wish, which constrains supply and growth and facilitates inflation.

Additionally, the employment rate needs to be raised by making it easier for young people to enter the labor market and by increasing the number of years spent at work before retirement, as neighboring countries have done. France has a very different employment rate at both ends of the life cycle, with about 35 percent of 60-64 year-olds employed compared to 62 percent in Germany or 70 percent in Sweden.

Education, both initial and continuing, must also become one of France’s strengths once again. International comparisons show that France’s training and education efficiency is decreasing despite a budget that is similar to or even higher than those of other European countries doing better in this regard (about 1 point of GDP more in France than in Germany). Here again, reforms are essential, even if the rise in the level of training can only be slow. The efficiency of education conditions the number of jobs as well as their qualification, which, in turn, influences the range of production and its quality-price ratio.

Finally, let’s not forget the reforms that enable productivity gains, which are essential for potential growth. France has made great progress in creating “tech” companies, and the Research Tax Credit (CICE) is a valuable example. However, it is important to note that the profit rate is a determinant of the amount of research and development carried out by companies. After being lower than neighboring countries for a long time, it has improved since the introduction of the CICE and the lowering of the corporate tax rate.

In contrast, public spending efficiency remains far below what is desirable. Despite being on the podium of public spending rates (about 8 points of GDP more than in Germany, 9 than in Sweden or 13 than in the Netherlands), France’s quality of public spending (including social security) is only average compared to OECD countries and is perceived as decreasing. This high level of public spending also results in a tax rate that is almost the highest in the world (more than 6 points of GDP above that of the euro zone excluding France), which is a definite handicap to competitiveness.

On top of that, compulsory levies, although very high, do not cover expenditure, which leads to a permanent public deficit and a permanently increasing public debt relative to GDP. As a result, our growth is obtained at the cost of an ever-increasing debt ratio, which is ultimately unsustainable. Since 2000, public debt in the euro zone has increased by 25 points of GDP, while France’s has increased by 50, twice as much. In the early 2000s, France’s public debt ratio was identical to Germany’s, at around 60%. Today, it is about 110% in France and 70% in Germany. Reforming the State and local authorities, combined with reforming the social systems, would help maintain the high level of social protection for the French and prevent it from declining.

Efficiency and respect for each person’s duty towards the common good of social protection are not a search for the lowest social standards, but rather the only way to preserve what is valuable for all. Ignoring or denying the usefulness of structural reforms would be playing with fire.