Dear Colleagues,

As you know, I will be relinquishing my functions at BRED on 31 May.

We have been working together for ten years now. And how much progress we have made! We have written some wonderful chapters in BRED’s story.

*

* *

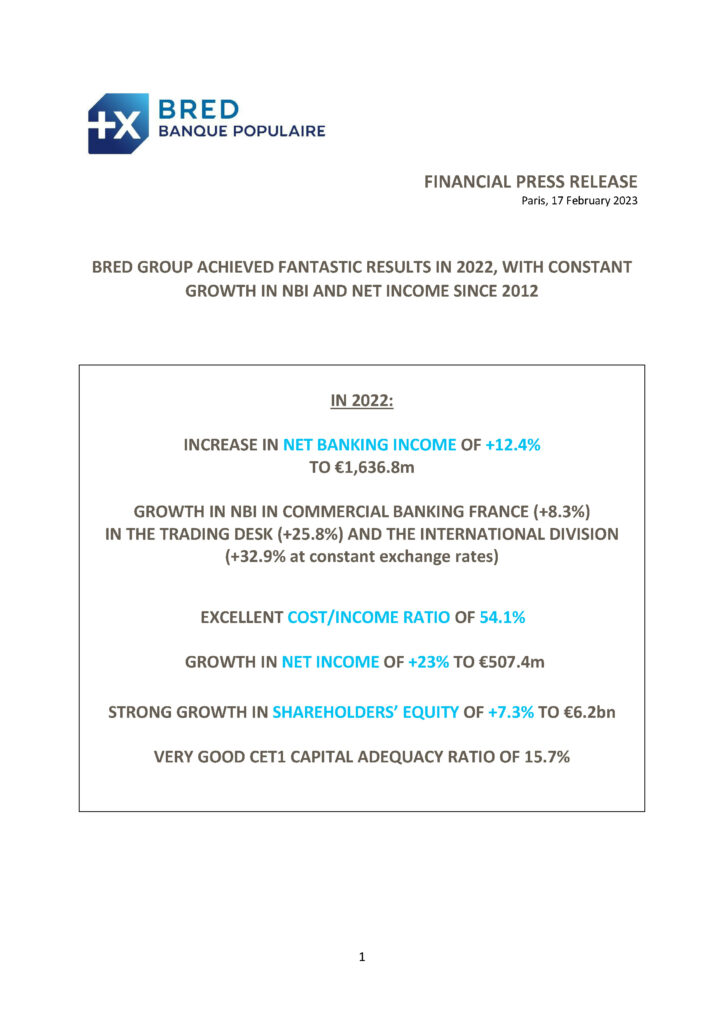

Ten years of success. We have posted historic results every year since 2012, continuously growing our NBI and net income. These results are not the fruit of chance; they are the result of the ongoing and renewed commitment of each and every one of you in implementing a strategy that has enabled us, year after year, to adapt to economic and social transformations, so that BRED always comes out on top. We addressed the challenge of the ramp-up of digital, not only through significant investments in tools to enable us to match the performance of our “pure player” competitors, but above all via the human aspect. We have invested in professional training, stepped up equal opportunities, and freed up our advisors by digitalising repetitive tasks in favour of a trustworthy and quality expert business relationship designed for the long-term.

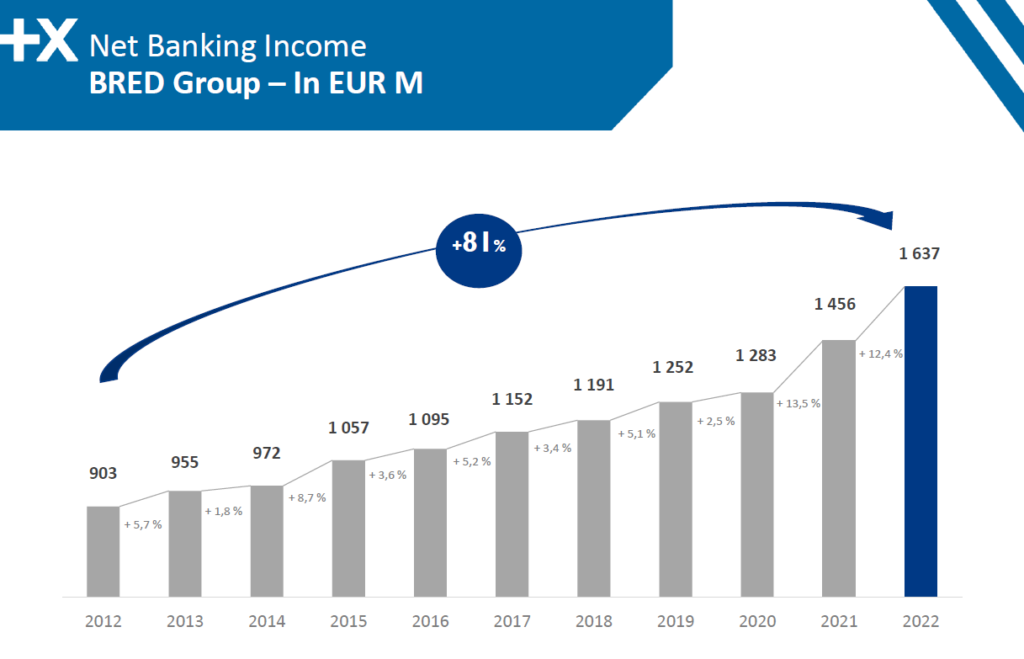

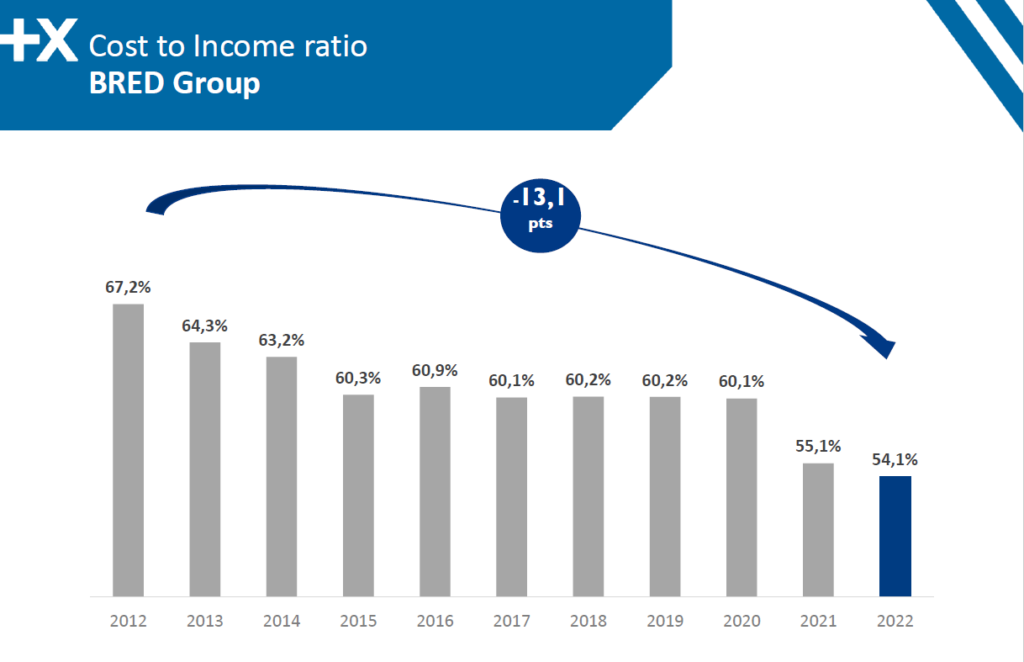

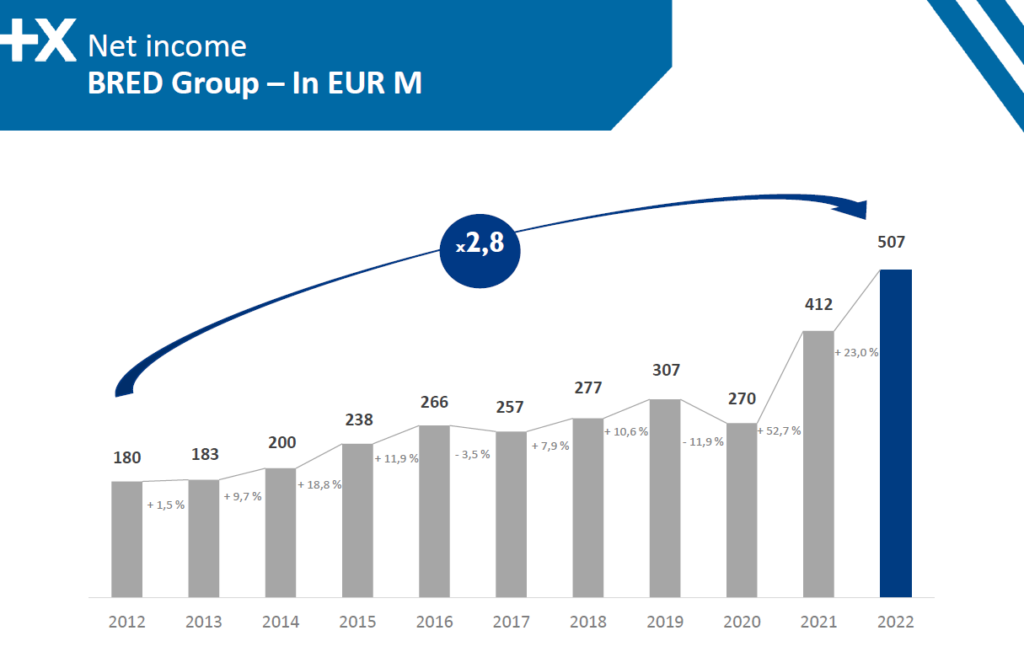

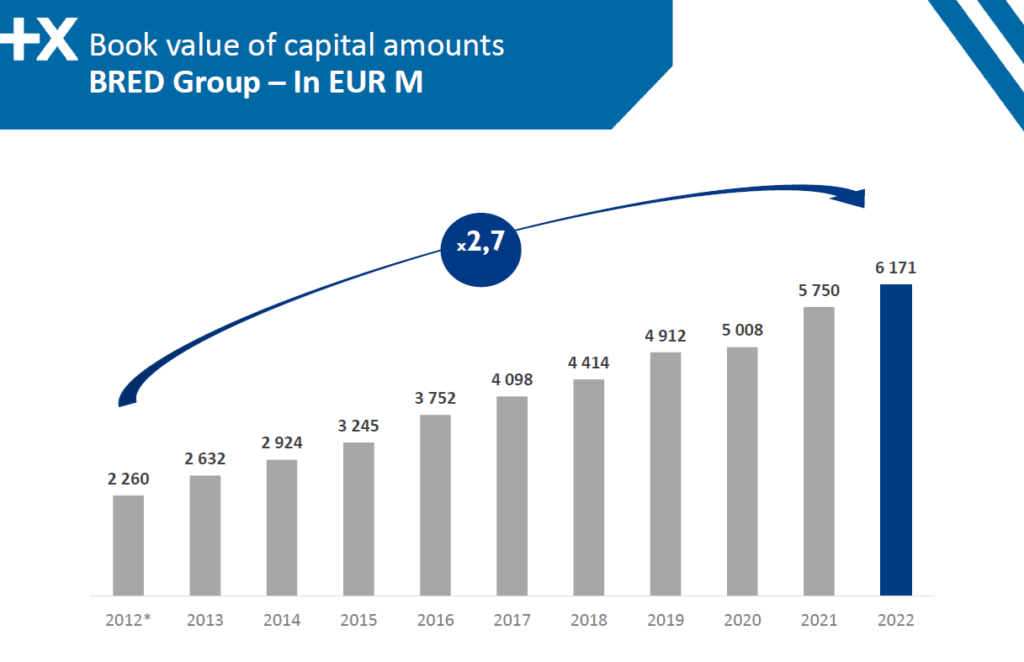

I am extremely happy that our BRED has forged ahead with this new model, a model of banking without distance and a promise to our customers of a global close relationship that abolishes both physical and behavioural distances by combining the best of the human and the digital. Firmly focused on the future, this loyalty to the fundamentals of the banking business has underpinned our success. The results speak for themselves: Ten years of growth, with an 81% increase in our NBI and a 2.7x increase in our shareholders’ equity; ten years of performance, with a 2.8x increase in our net income; and ten years of continuous improvement in our efficiency, with a 13.1- point decrease in our cost/income ratio to reach an outstanding level of 54%. These results are not a self-congratulatory obsession – they are the real-lie illustration of how BRED, across its various businesses, has met the expectations of the market and successfully gained the loyalty of its customers. Our results have also been marked by the confidence granted to us by our members, the number of which has risen 47% in ten years. Bravo to us and to you. On the back of these results, profit sharing and incentives have also increased spectacularly, by a factor of 2.3 since 2012.

*

* *

Yet the climate has not always been favourable to us – far from it. In a low interest-rate environment for banks, we succeeded in outperforming. And how could I not mention the unprecedented situation we experienced during the pandemic? Amid a threefold, health, economic and financial crisis, our results testified to our resilience and the relevance of our trajectory, as well as our ability to succeed in the challenges having faced commercial banks for many years now.

This period considerably accelerated the major changes under way and required companies to reorganise quickly. It encouraged BRED to go even further in banking without distance and switch to 100% advisory banking. The solidity of our bank also enabled us to support the economic recovery of our country, and this is something we can be proud of.

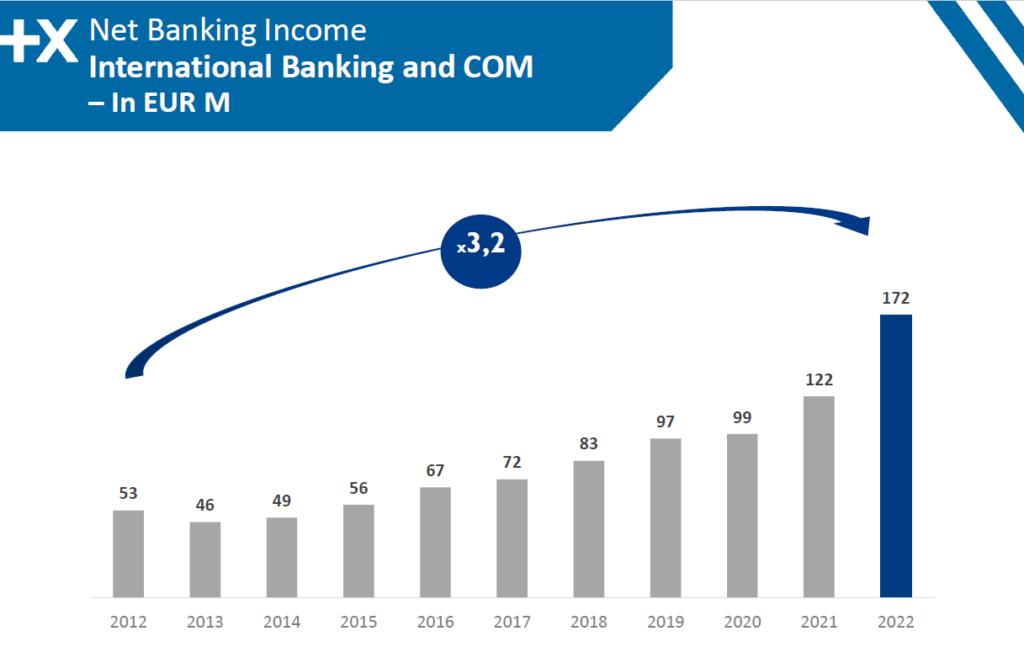

The relevance of our strategy also extends far beyond our borders. In the last ten years we have pursued our international expansion and created new banks in dynamic countries, with the unwavering determination to provide expertise and added value commensurate with the highest international standards. We are now established and growing strongly in Cambodia, Laos, Fiji Islands, the Solomon Islands and Vanuatu; we are the number-one bank in Djibouti. Our international trade financing business launched six years ago in Switzerland and more recently in Dubai has proved an enormous success. These achievements can be seen directly in our performance, with international business contributing 16% of our NBI in 2022.

*

* *

More than results, I have experienced a magnificent human adventure by your sides. From my time at BRED I will always remember our incredible collective power during tough times, as well as more joyous times that we shared at regional conferences and across the entire BRED Group. A particularly special memory for me was our 100th anniversary celebration at the Grand Palais, an exceptional event in all senses of the word, and one that I will never forget.

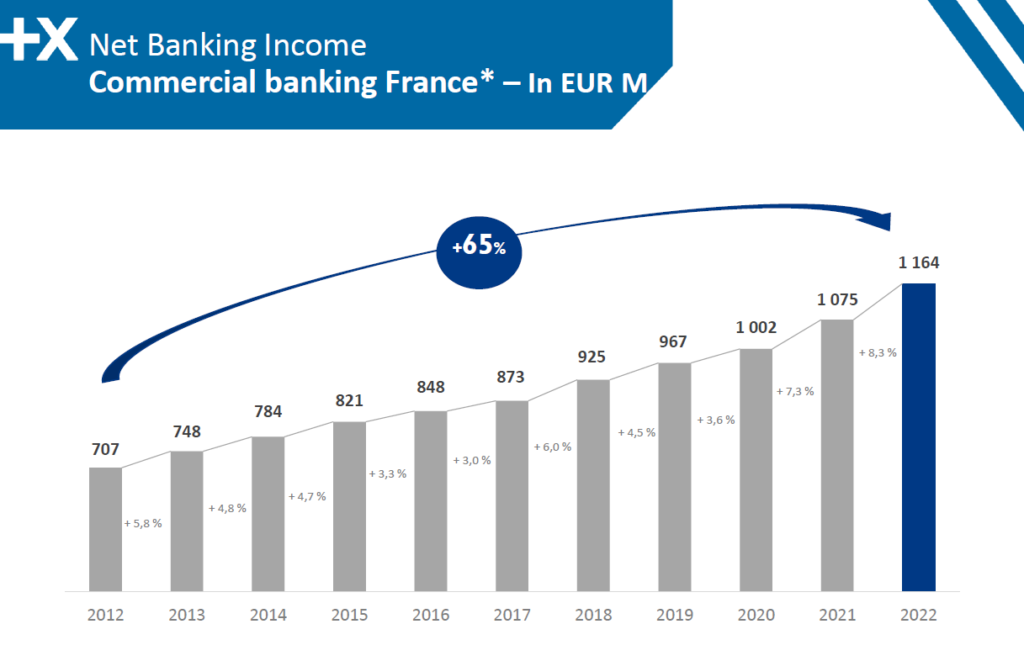

I am thankful to have worked with motivated, passionate and committed teams and to have been part of absolutely remarkable achievements across the division in France, including in mainland France, Guadeloupe, Saint-Martin-Saint-Barthélemy, Martinique, French Guiana, Reunion and Mayotte. All our business lines have put in strong performances: our branches and business centres, and our Private Bank, rated as the best private bank in France in 2022. Our Corporate Banking Division has taken on true stature and succeeded on the strength of its know-how and technical expertise. Our trading desk was recognised in late 2022 as the best European bank for placing the short-term debt of major European issuers. Last but not least, our international banking business, which has undergone tremendous structuring and development. Our BRED has also been acknowledged for its CSR performance, gaining an extremely high-level Sustainability Rating (A1) from Moody’s.

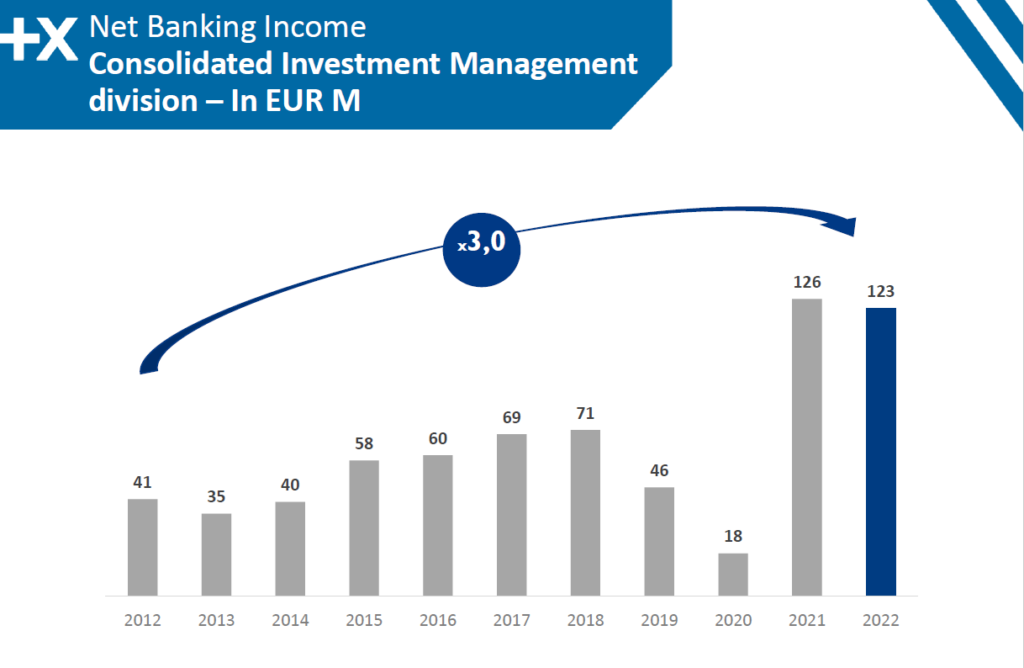

Our Promepar, Cofilease, Prepar-Vie Assurance, Sofider, Adaxtra, Ingepar and Vialink subsidiaries continue to step up their development and the distribution of their wide-ranging offers. They have now been brought together at a new building in La Défense.

Bravo to all ! Ten years of success in which we have enabled BRED to always come out stronger while many groups have aimed to get by through substantial cost-cutting.

*

* *

As I say my goodbyes, I would also like to remind you that our banking profession is passionate, and even essential to the economy, regions, and people themselves.

I have made economics my life, because I see it as the queen of the human sciences. Economics tries to explain how people organise themselves to live, to form a society and seek to improve their lot. And from my passion for economics has come my passion for banks, the place where we can best observe and act on the economy.

A bank is above all a business, with a strategy, resources, objectives and a corporate purpose. To my mind, running a business is first and foremost a responsibility towards its constituent teams. Over these ten years, my unfailing question has been to ascertain whether everything has been done for BRED to move in the right direction, to be profitable on a lasting basis to protect jobs, so that working here is both an individual and collective achievement, and so that we take pleasure in our work and are proud of belonging to the bank. I have always endeavoured to be fair and ensure that everyone else is, because a fair business is a guarantee of job satisfaction and success. It is a business that provides equal opportunities – the same opportunities for everyone, regardless of their, gender religion, skin colour, social origin or educational background. And as I have said on numerous occasions, for me it is a question of combining efficiency and ethics, both with regard to employees and to customers and society. Both are necessary. Efficiency without ethics does not work for long, while ethics without efficiency cannot exist because there are no means to make it work.

I hope with all my heart that you share the idea that our work as bankers has meaning, that what we do is useful, because as commercial banks we are absolutely indispensable to the economy and to the individuals, thus to society as a whole. What a marvellous job we have! We support and facilitate the life and business projects of our customers, over the long term. We are a relational bank, an advisory bank, in the long term, with trust.

We are also the parties that match financing capacities with financing needs. To do so, we take on the credit, interest-rate and liquidity risks instead of leaving them to be borne by households and businesses who are unwilling or unable to take them. And at BRED, a cooperative regional bank, we are crucial to the regions in which we operate, both in France and internationally, as we are tied to them through convergent interests. There is a true osmosis between our territories and ourselves. If the territory is doing well, the bank is doing well. And if the bank is doing well, the development of the territory will go well. So the concept of CSR is even more real and concrete. Our bank is truly committed to each of these territories. First and foremost by doing our job well, which is essential. And through our investment in favour of equal opportunities, as well as culture, which are powerful drivers of social cohesion and, hence, well-being. In a highly globalised world, we have seen the emergence in recent years of an even stronger need for closeness, a need to which I feel that we respond.

For all these reasons, commercial banks, and BRED, are essential. And rest assured: we have a wonderful future ahead. Because our mutual and cooperative model enables a fruitful alliance of efficiency and ethics, I am convinced that we will be around for a long time to come. We prove this every day and in the long term, even though people have for years been announcing that traditional banks will give way to new competitors. But this position is often based on a false understanding of the essence itself of banking, the forecast demise of which is overly hasty. At BRED, despite the health, financial and economic crises, despite the emergence of low-cost online banks, despite cryptocurrencies, despite excessively low interest rates for an excessively long time and despite all the obstacles in our path, we have not reduced our workforce. On the contrary. Neither have we closed branches – again, on the contrary. Our results have not slipped; they have nearly tripled in ten years. We have come out strong because we are committed together with efficiency and conviction in a strategy that has succeeded and continues to deliver. And to remain strong, to continue to make headway, we need to make the necessary changes while safeguarding the essence itself of our banking profession. We need to maintain our momentum, our talent for overcoming obstacles, our fighting spirit and the pride we have in our profession, and in our bank. This is absolutely essential.

*

* *

We have experienced ten years of collective success. I am certain that you will continue to successfully write the story of our wonderful company, that you will stay your course through a rational management approach underpinned by the strengths and values of the BRED Group, namely value-added advice, close relationships with our customers, a proactive approach and entrepreneurial spirit.

And I am certain that you will find the same values with my successor, Jean-Paul Julia, recruited in 2015 to head Corporate Banking, and who then went on to become Chief Executive Officer of Banque Populaire Bourgogne Franche-Comté. Jean-Paul has extensive knowledge of BRED and its business lines.

In the coming years, I wish you as much pleasure and at least as much success as we had together.

Thank you all. Thank you for your determination, your talent and your sense of individual and collective success. Thank you to Stève Gentili and Isabelle Gratiant, and the entire Board, for having enabled me to bring together everything I admire in banking: retail banking, private banking, corporate and investment banking, capital markets banking, and international banking. And thank you for having unwaveringly supported the integrity of our bank, while ensuring benevolent and exacting supervision. You have made my adventure at BRED the most wonderful experience. We can be extremely proud of what we have achieved together.

Long live BRED. And long live you!