Following the European elections, “populist” parties have gained in power but failed to make a sweeping advance. They have increased their number of MEPs from 205 to 210, ahead of the probable departure of 34 from the UK.

At an average 51%, the participation rate in 2019 was the highest since 1999.

Attachment to the European Union remains strong. Surveys show that 50% of the Italian population responded positively, compared with 52% for France, 67% for Spain and 70% for Germany. Even though confidence in (rather than attachment to) the European Union dipped substantially between 2007-2008 and 2014-2015. Between 20% and 35% depending on the country, at the end of this period. But confidence has risen slightly since (between 30% and 50% depending on the country). And the percentage of the population thinking their country would fare better outside the Union has decreased since 2013. Around 20% for Germans and the Spanish, 30% for the French, and over 40% for Italians.

The percentage of people favourable to the Euro is stable overall. Around 80% for Germans and the Spanish. Over 70% for the French. And over 60% for Italians, though this percentage has fallen sharply since 2000.

While immigration remains a concern, the four countries we studied were, by a large majority (70% to 90%), favourable to a common migration policy.

But dissatisfaction concerning the functioning of democracy in the Union has risen over the last 20 years, notably since 2012, the dissatisfaction rate today standing at around 50%.

So the major disruption failed to occur. And the idea of Europe and the Euro are holding up strongly in the hearts of the Union’s population. However, we think overly hasty celebrations would be dangerous. Granted, even the “populist” parties no longer boast about wanting to quit the single currency or the EU. But the forces behind the rise of these parties in a number of European countries are still at play and the underlying reasons still very much a reality.

One of those reasons, one that has been thoroughly analysed, is the combined effects of globalisation and the technological revolution, which has led to the declassification and relative impoverishment of the middle classes, or a fear of such. This phenomenon is not reserved to Europe; many other countries are seeing a rise in anti-system and anti-globalisation movements.

However, the decreases in the surveys mentioned above occurred in the EU mainly starting in 2010-2012, i.e. at the time of the eurozone-specific crisis and its defective management. The issue of improving the functioning of the eurozone remains insufficiently examined. And a new crisis would undoubtedly be dangerous, with increasingly costly political and social consequences.

Immigration is also a subject that still needs to be discussed and shared within the Union.

The call to order issuing from the survey on the need for the improved democratic functioning of the Union is not a chimera. As things stand now, institutional reform will not suffice; what is needed in reality is a feeling of stronger proximity between Europe and its inhabitants. Notably through active cooperation implementing European industrial, technological, defence and ecological projects. Even if each of these projects fails to unite all the EU countries. These achievements, the result of collaborative efforts between European businesses, and wherever necessary backed by the EU budget, would help everyone to better perceive the usefulness of Europe in the economic and social life of their territory.

Lastly – and we can all see the growing urgency of this point – the Union of European Nations must also become a strategic Europe. Only such a Europe would be able to play a full role in the new global power balance that is being forged before our eyes, leading today to an unstable confrontation between China and the United States, and from which Europe is dramatically excluded.

As such, defending the European idea today can no longer essentially consist in complaining about a lack of communication or lamenting that its detractors are distorting the truth. Neither can it be based on simply repeating the need for greater integration via the gradual relinquishing of sovereignty. Like it or not, in our current circumstances, this attitude seems to be producing the opposite of the desired goal.

We should thus refrain from seeking the impossible, and instead take an unflinching look at the unresolved problems and intrinsic defects of European construction as it stands today. We should pragmatically seek out any possibility of reviving cooperation topics and processes between the Member States and European players, to achieve together what no-one achieve alone.

After all, would this not be tantamount to updating the principle of subsidiarity dear to Jacques Delors? Now more than ever, what the people want is for Member States to not be stripped of their identity or sovereignty regarding any matter that they can manage themselves. And institutional progress is currently not on the agenda of a number of EU countries. Through new or revived collaborative efforts between European countries, it is vital to enable citizens to open up more possibilities. And, as part of a supplementary rather than substitutive identity, it is crucial to offer them greater control over their destiny. Could this be the start of the rebirth?

The European League must take an active part in this debate and devise new ideas. This ability to be committed and useful hinges on each one of its members. Your support is necessary if, in a manner both pragmatic and critical (and in the full sense of the latter word), we are to contribute at our level to reviving Europe. We need to seek out and promote concrete pathways to go beyond today’s blockages. In short, we need to renew the ideal. The recent elections give us hope that this is possible.

With the first country ever having decided to leave the European Union, a sentiment of distrust appears to be on the rise, along with a waning of interest in integration, an increased need for identity and the resurgence of the nation state.

North-South tensions in the eurozone are rising, with Southern countries denouncing the lack of solidarity on the part of Northern countries and Northern countries feeling that Southern countries are not rigorous enough for them to show solidarity and share their economic risks. Can a strategic Europe still emerge to take a place between the United States and China and to bring our vision to the table as part of the reshuffle of the global power balance currently afoot?

Is there a possibility, a realistic path, of combining a sovereign Europe and a Europe of nation states – to which there is currently no alternative – to forge a successful outcome to a situation of great concern today for convinced Europeans? What new compromises are possible for pursuing European construction? And what new institutional arrangements are required to protect the eurozone in the event of a new crisis?

Through our events, the French Section of the European League for Economic Cooperation, which I have chaired since January, succeeding Philippe Jurgensen, who now serves as Honorary Chairman, is seeking to find answers to these questions and present them independently to political and economic decision-makers. It is more vital than ever to explain the benefits of Europe. But it is equally vital to address the necessary changes and rebuild in-depth dialogue between the various players and countries of Europe so as to keep from falling into a rut or, worse, disintegrating.

The two sessions of “citizen consultations” organised by the League in September and October were key events in 2018, bringing together some 100 participants, including experts and non-experts from diverse fields and featuring three renowned economists, Agnès Bénassy-Quéré, Patrick Artus and Xavier Timbeau. The aim was to debate desirable and realistic improvements in the eurozone with the European elections on the horizon. Through the event, we were able to develop and send proposals as part of the framework provided for by the head of state.

A number of working lunches and breakfasts, as well as special theme-based committee meetings, were organised in 2018 focused on personalities and topics enabling us to further our understanding of Europe’s strengths and difficulties, and desirable or possible changes.

The French Section of the European League for Economic Cooperation is an open space for debate and dialogue which, to be as useful as possible to the defence and promotion of Europe, requires the active contribution of each of its members. It also needs to grow its membership – of private individuals and companies alike – to boost its reach, i.e. its ability to weigh in debate and promote a responsible and socially-minded Europe, a Union attached to democratic values and those of an open society founded on the rule of law, in which social aspects are combined effectively with economic aspects. A Europe with a strong strategy, enabling it to keep the world from becoming locked into an economic and diplomatic face-off between the United States and China, which would relegate our continent to the role of powerless spectator.

Through our ideas and common energy, let us make our best contribution to finding the right solutions for Europe, both here and elsewhere.

I would like to thank each one of you for being a member of the European League for Economic Cooperation.

LE CERCLE – France has one of the lowest levels of income inequality, observes Olivier Klein, professor of economics at HEC. But inequality of opportunity in France is much higher than in other OECD countries.

Inequality is a central issue in many countries. In order to know how to take effective action and to avoid exacerbating the situation with inappropriate policies, the proper diagnosis needs to be made.

France has a high rate of income inequality compared to comparable countries. However, owing to a redistribution policy that is among the most extensive of OECD countries, France ranks, after redistribution, among the countries with the lowest income inequality.

This finding is confirmed if we analyse the share of national income received by the richest 1%. While it has tended to rise a little over the years (rising from 9% to 10.5% in 20 years), this increase nevertheless remains far more limited than in neighbouring countries. Over the same period, it has increased from 9% to 13% in Germany, while in the United States it has risen from 15% to 20%. Likewise, the percentage of the French population that lives below the poverty level is not only less than that of most European countries, but it has also been decreasing for 20 years.

Inequality of opportunity

However, while France ranks among the countries with the lowest income inequality, inequality of opportunity is higher in France than in similar countries. According to the OECD, it takes on average six generations for a family at the bottom of the income scale in France to reach the average income, while it takes only two generations in Denmark, three in Sweden, four in Spain and five in the United States.

We can draw two thought-provoking conclusions about the current social environment from these statistics. Against a backdrop of globalisation and digital revolution, innovation appears to be a critical competitive factor for developed countries. As such, knowledge and innovation are directly associated with reduced inequality of opportunity, because innovation is a growth factor and therefore helps to combats poverty. It is also disruptive and shakes up the status quo, which enables the most talented to progress and improves their social mobility, thereby providing better social fluidity.

Vicious Circle

Secondly, while redistribution is very honourable as a collective choice, at that level, it creates a vicious circle. A level of social security contributions much greater than the European average impedes competition. In France, this situation contributes to a low employment rate which, in turn, causes higher income inequality before redistribution, which leads to very high levels of redistribution, over and over again. And the low employment rate and the levels of long-term unemployment lead to greater inequality of opportunity.

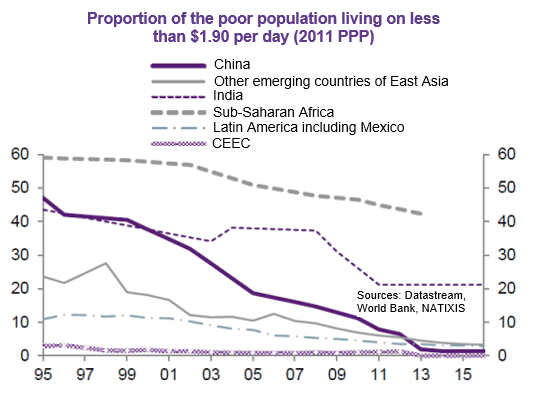

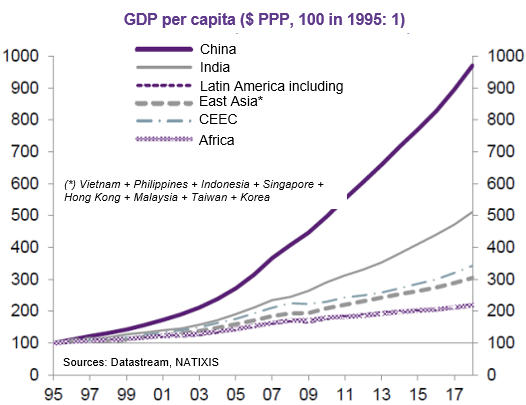

By nature, the topic of inequality covers several aspects. If we look at the global level, levels of inequality between poor and rich countries have decreased considerably since the 1980s. According to the World Bank, 40% of the world’s population in 1981 lived below the extreme poverty line compared with only 11% today. The growth rate of emerging countries has therefore substantially reduced inequalities between the average living standards of the various countries. And if we focus on just China and India, which have experienced and continue to see the strongest economic development since the 1980s, 2 billion people have risen above the poverty line. That’s great progress and one of the obvious benefits of globalisation.

That’s true not only for income, but also for health. My data are less recent, and it has improved even more since then. In 1940, life expectancy in developing countries was 44.5 years. In the 80s, it reached 64.3 years. That’s an increase of 20 years over this 40-year period. Meanwhile, people in developed countries are living nine years longer. Here again, we can see that inequalities in health and life expectancy have decreased.

On the other hand, inequalities within each country, whether developed or emerging, have increased on average with globalisation and growth. That’s because although the growth process allows the greatest number of people to increase their standard of living, some in each country are progressing faster than others, and in some countries, people at the top of the pyramid have access to a larger share of national income. The standard of living has therefore increased for nearly everyone. However, inequality has still managed to grow, simply because certain people’s situations have improved more quickly than others. That’s the nature of happiness, measured by economists in an informative way. All the studies show that happiness is relative. We’re happy when we’re doing better and when our situation improves faster than others. In other words, by comparison. In relative terms. So, even though everyone’s standard of living is rising, the increase in inequality is quickly becoming a social and political topic. We’re therefore seeing a phenomenon needing better clarity: dramatically smaller inequality between countries and growing inequality within countries, even though the level of wealth and well-being has increased overall.

The issue of inequality can therefore be addressed and analysed in various ways.

Income inequality can be measured by looking at the share of the country’s income held by the top 1%. Inequality can also be measured much more precisely and undoubtedly with more relevance with the Gini index. Gini was an economist and statistician who invented the method of studying the distribution of inequality across the entire population. We look at the differences between everyone two by two and average the differences from each to each. If the average of the differences is zero, that means that everyone has exactly the same income. An average of 1 means total inequality. These indices are measured across all OECD countries.

Lastly, a third way doesn’t look at income inequality but at inequality of opportunity. Of course, we’re talking about social mobility and the “poverty traps” that generations can fall into. Equal opportunity is obviously crucial because it relates to the republican pact, the social pact, and the ability to live together and obviously because it is fundamental for the health of a society and its cohesion. When inequality of opportunity is low, more people can be mobilised. That means that no matter where you’re born, if you have talent and equal opportunities, you’ll manage to advance. So, not only is the belief that everyone has the same opportunities an important factor of social cohesion, but it also helps to foster growth because it mobilises all talents wherever they are. The issue of inequality of opportunities is therefore crucial. It means knowing whether they are still the same and their children who all have their opportunities to succeed or if the pathways can be fluid without too much determination for the original social environment. And we’ll see that in France, there is a strong adhesion at both the top and the bottom.

Findings: I’ll start by presenting a few figures and then some analysis.

In France, compared with neighbouring countries, income inequality after distribution is rather low, whereas income inequality before distribution is rather high. Meanwhile, inequality of opportunities is rather high.

We’ll use these findings to try to come up with some possible conclusions in terms of economic policy and necessary reforms.

First, let’s take a look at the measurement of income inequality before distribution and after distribution. Before allocation, it’s clear, for example, that inequality is greater if wages range from 1 to 1,000 rather than 1 to 100. But we also have to consider people who aren’t working and therefore have very low incomes. The more people there are excluded from employment, the greater income inequality before redistribution is. And the more powerful the redistribution system is, whether through taxes, support income, and or other ways, the lower income inequality after distribution is.

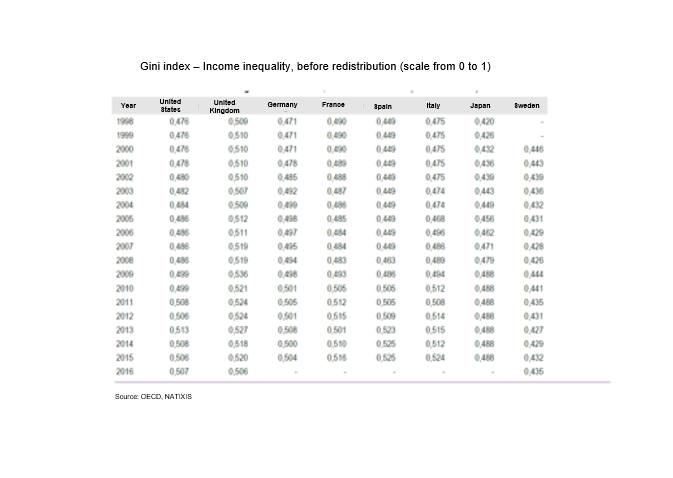

Before distribution, the GINI index rose from 0.477 in the United States in 1996 to 0.507 in 2016. In the UK, contrary to what one might think, there has been little increase. It increased from 0.473 to 0.504 in the EU and from 0.409 to 0.488 in Japan. So, what do we see? Inequality has actually risen everywhere. And in the US, it hasn’t risen much more than elsewhere, before distribution. Its level of inequality isn’t really much higher than in the eurozone, while in Japan it’s lower.

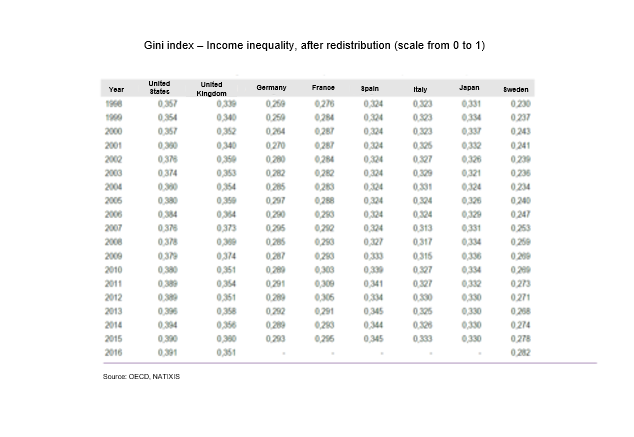

After distribution, the US fell from 0.507 to 0.391 in 2016. We can therefore see the effect of distribution. It clearly reduces income inequality. There has been a sharp decline in the UK as well. After distribution, the eurozone is a much more egalitarian system than the US since it’s much lower after distribution there. Europe therefore has a system that does more to reduce inequality. And Japan lies between them.

Let’s analyse France. Before redistribution, the Gini index rose from 0.490 in 1998 to 0.516 in 2015. That’s a fairly small upward trend in inequality. Are these inequalities big or small compared with other countries? In 2015, France was a little more unequal before redistribution than the US. Is it because there’s a broader range of wages? Of course not. It’s because there are many more people out of work. That’s an essentially French problem. Other countries very often have an employment rate 10 points higher (75% compared with 65% in France). Germany is almost at the US level. And we know that the unemployment level is very high there. Spain’s level of inequality before redistribution is even greater than France’s. Not surprisingly, Sweden is a more egalitarian country even before distribution. We can therefore see that France had high levels of inequality before redistribution.

But after redistribution, what’s the finding?

In 2015, France was at 0.295, one the lowest indices of all the countries considered. That means it went from having one of the highest indices in terms of inequality before redistribution to one of the lowest after redistribution. We can therefore see that redistribution is very strong in France. In the US, the level of inequality after redistribution is much higher than in France. But in Spain, Italy, and Germany, the level of income inequality after redistribution is about the same as in France. And France’s levels, again after redistribution, are quite comparable to Sweden’s.

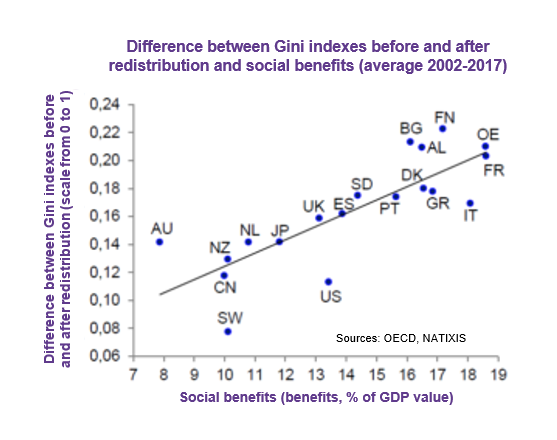

France thus has a one of the highest redistribution policies, relative to GDP, of all OECD countries. The advantage is reduced inequalities, but there are also disadvantages. It means much higher taxes and mandatory contributions, which is not without consequences. We can easily see a correlation between the Gini index after redistribution and the burden of social benefits relative to GDP. And, thanks to one of the strongest redistributions among OECD countries, France has one of the lowest income inequalities. Only Denmark, Finland, and Sweden have lower levels.

Now let’s consider the proportion of national income received by the 1% of individuals with the highest national income. In France, they received 9% of national income in 1995. In 2015, they received 10.5%. For the sake of comparison, Sweden had the lowest percentage at 6% of national income versus 9% in France in 1995 and 8% versus 10.5% in 2015. That’s not a huge difference. Let’s look at the United States. In 1995, the richest 1% received 15% of national income. In 2015, this figure was a little over 20%. That’s clearly a striking figure. It’s twice as much as in France. And the increase in the share received by the richest 1% has been much more brutal. In Germany, growth has been a little stronger than in France. While it was also 9% in 1995 like in France, it was 13% in 2015. However, we’re very far from the US. All in all, the richest 1% have received a growing portion of national income. But the phenomenon is much more visible in the US than in Europe.

Another way to analyse inequality is to look at the percentage of individuals at the poverty line.

The customary international way of calculating it can be called into question, but at least it’s an indicator used everywhere. We look at the median income of the French or Americans, for example, as a percentage. Anyone under 50%, or 60% like in our figures on this medium income, is considered poor. It is a relative notion of poverty.

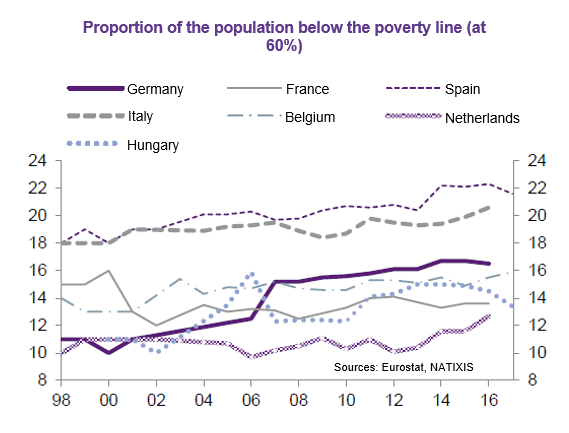

In France, few people are below the poverty line, meaning below 60% of French median income. Meanwhile the percentage is higher in Spain and Italy. It’s also higher in the US. And the percentage of the French population under the poverty line even decreased between 1998 and 2016. It increased in Germany over the same period. So, again, we can’t say that poverty is high or has increased in France. What we sometimes hear in the media is simply statistically false.

However, in France, inequality of opportunity is rather high compared with similar countries.

According to opinion polls conducted by the OECD, 44% of French respondents believe that education passed down by parents is important for progress through life. In the OECD, which includes Chile, Mexico, all European countries, the United States, etc., the average opinion is at 37%. This reflects a rather high sense of inequality of opportunity in France. Unfortunately, this opinion is correct. In France, socio-economic status is passed on more strongly than elsewhere from one generation to the next. The relative income level is passed on more strongly from one generation to another than in other countries. Lastly, the level of education and diploma is passed on more strongly from parents to children than in other countries. According to these three criteria, inequality of opportunity is greater in France than elsewhere.

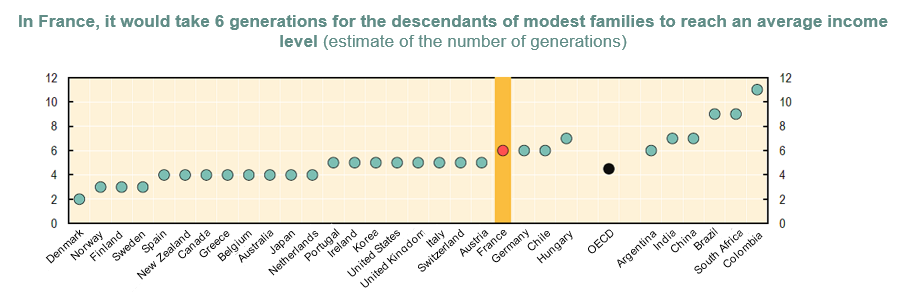

Of course, inequality of opportunity exists everywhere, since the socio-cultural environment is very important in the life and development of children. But the way we manage to partially correct the phenomenon can be more or less strong. The OECD calculated this and published a report on this subject, taking intergenerational mobility into account. Then we look at how many generations it takes for a family at the bottom of the ladder to reach the middle range. Clearly, the fewer generations required to reach the average, applying the average mobility of society, the less inequality of opportunity there is. The more generations it takes to achieve this, the more one is confined to the bottom of the ladder or symmetrically protected at the top of the ladder.

In Denmark, it takes 2 generations. In Norway, 3; in Finland, 3; in Sweden, 3; in Spain, 4. In New Zealand, Canada, Greece, Belgium, Australia, Japan, and the Netherlands, 4. In the United States, 5.And in France, 6.

Six generations so that someone at the very bottom of the income ladder has a chance that their great grandchildren will reach the middle income level, given French mobility. Germany doesn’t do better, and neither does Chile! And the average for the OECD is between 4 and 5.

Studies have reached the same conclusions about the inequality of opportunity in France, relative to comparable countries, by calculating the correlations between the income of parents and the income of children once they reach adulthood. The findings regarding correlations of diploma level are similar.

What structural reforms should be done to combat inequality of opportunity?

Of course, the reform of national education must be mentioned. There is currently much less mobility and equality of opportunity in France than many years ago when teachers who supported and pushed their deserving pupils were called “horsemen of the Republic”. This state of mind has not been abandoned, but it is much less widespread, and in reality, national education has declined in overall effectiveness for many reasons that can be explained more or less easily. The effectiveness of education is measured and compared using level tests carried out internationally by the OECD.

Comparative studies show that national education must be able to devote slightly more resources to children in disadvantaged areas or neighbourhoods. It’s also known that a lot comes into place early in life, in kindergarten, and in elementary school. That’s where more resources are needed. But let’s not fool ourselves. It’s a question of efficiency and not global means within national education in France, which has a much higher budget-to-GDP ratio than the other European countries for a disappointing result in the tests. People also must be supported during their career so that they can progress. Professional training in France is very inefficient and is in the process of being reformed.

Some countries do all this remarkably well, such as South Korea and the Nordic countries. They equip themselves with the means to ensure a good degree of social mobility in their country. Once again, that’s useful, not only for social cohesion, but also for the economy because there will be a search for talent that otherwise wouldn’t be able to express themselves and obviously contribute to the general growth.

In addition, long-term unemployment needs to be reduced, which means more effective support for returning to work and better incentives to take up a job. We also know very well that people in France are entitled to unemployment after four months of work. It’s one of the few countries where it takes so little time to be entitled to unemployment. That should be looked at. And, of course, we contributes to the creation of jobs must be facilitated…

It’s also important to work on territorial inequalities, because they exist.

So, there’s generally less social mobility in France than in other comparable countries, and this is reflected in the evolution between generations through income, degrees, and socio-professional categories.

Plus, we know that low mobility is not only intergenerational, but there is also fewer chances in France than elsewhere for people to be able to evolve during their life.

Two analyses:

From all this, I feel that there are two analyses that need to be given thought.

The first is the link between growth, innovation, and equal opportunities. The second is strong redistribution, which greatly reduces the initial inequalities that lead to a vicious circle.

First angle of analysis is the link between growth, equality, and innovation. For 20 years now, we’ve been living in a context of globalisation and a technological revolution related to digital. These two phenomena are increasingly eliminating repetitive work and the corresponding jobs.

Today, growing in an economy that is no longer a catch-up economy like in the post-war year requires being innovative. Innovation is crucial as the current driving force behind the growth of countries at the “technological frontier” (1). Emerging countries are catching up to developed countries, which must innovate constantly to continue to grow as emerging countries grow very quickly.

That means that we’re in an economy of knowledge and innovation – the only way to create growth and wealth.

As a result, we have to make sure to encourage innovation in our economy and our institutions (for example, organisational methods, labour market, and legislative framework). There’s also a link with equal opportunities because it’s obviously easier to fight poverty when there is growth. And it’s also easier to ensure social promotion to provide social mobility. If we step back and look at ourselves as a company rather than a country, we know that in a company that doesn’t develop, it’s very difficult to develop employees and help them grow. In a growing business, all those who are motivated and talented can be helped to grow.

Growth is therefore needed to reduce the inequality of opportunity and permit social promotion and mobility. If we don’t have enough growth and innovation, we end up with a blocked or jammed society and insufficient social mobility, and this leads to many social cohesion problems. In addition, as I already mentioned, the more we manage to promote equal opportunities, the greater the number of mobilised talents will be, and their energy will contribute to growth. So, we see the virtuous link between these different factors.

Plus, innovations create breakthroughs, which then create new sources of growth and wealth. Innovation therefore calls into question accrued benefits. And that’s also what enables social mobility. In the US, if we suddenly see people appear in the wealth rankings and develop new businesses very quickly, it’s because they seize innovations and can experience some amazing personal developments.

I’m not saying that this is a model in itself, but simply that, even at smaller scales, it’s essential. The more innovation, capacity to invest, and growth there are, the more it is possible to go beyond pensions and promote social mobility.

We therefore have to know how to ensure policies that facilitate innovation and promote this phenomenon. Once again, the innovation economy is the economy of knowledge: it’s education, it’s professional training, and it’s the promotion of all talents. It’s also means eliminating “poverty traps” by, as I already mentioned, better incentives to work, better support in finding a job, and easier abilities to switch jobs in shifting economies.

And that too is part of the necessary structural reforms. To encourage technical progress and innovation, competitiveness must also be encouraged through investment.

The second area of thought is the analysis of income inequalities before distribution and after distribution and the cost of this distribution (2).

The rather high income inequality before distribution is offset in France by redistribution, which is a strong redistribution because inequalities aren’t liked in France. In a way, what’s honourable is a collective choice. But a strong redistribution has a high cost in terms of social benefits and naturally social contributions and taxes. And because this leads to a lot of levies on companies, it spills over onto competitiveness. And lower competitiveness translates into fewer jobs. And the loop goes on. Because if there are fewer jobs, there are much stronger pockets of poverty and therefore large income inequalities before distribution. And then there’s long-term unemployment that must be offset by more redistribution and therefore more business costs. This leads us into a vicious circle.

The goal should therefore probably be to avoid over-repairing. Repairing is certainly normal, but better still is to do better upstream, to reduce income inequality before redistribution and avoid falling into this vicious circle. Prevent rather than repairing a lot of things.

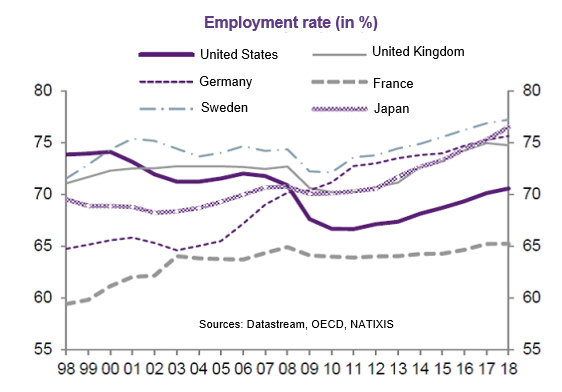

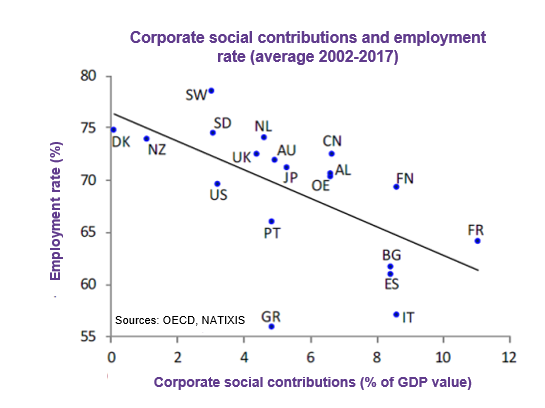

The employment rate in France is 65%. That’s around 10% lower than in comparable countries. This is an unacceptable situation in itself. In France, there aren’t enough working-age people who are working. If we consider the two extremes, between the ages of 60 and 65, there are far fewer people working in France than elsewhere. Much fewer than in Germany, not to mention Sweden, in comparing France to countries with comparable models. Similarly, it’s very difficult for young people to find a job. And we can see the correlation: the lower the employment rate is, the higher the social benefits needed to offset the created inequalities.

Now let’s consider the correlation between employment rates and the size of distribution policies. In other words, employment rates and differences between the GINI indices before and after distribution. France has the strongest redistribution policies and the lowest employment rates.

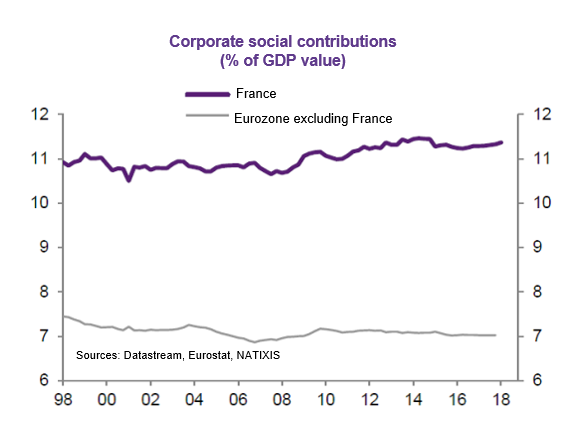

Again, the correlation is obvious for OECD countries. Because of France’s significant redistribution policy, its social security contributions are roughly 60% higher than the eurozone average and therefore the contributions of neighbouring and comparable countries.

Companies are therefore structurally less competitive. After social contributions, there are left with a considerable disadvantage in terms of the overall cost of labour. This then means a lack of jobs, resulting in large income inequalities before redistribution. Hence the fact that we redistribute strongly… I don’t think redistribution should be stopped. That’s not my point at all. But to do sound, normal redistribution that doesn’t cost in terms of growth and jobs, we must strive to allow many more people to work and therefore allow our businesses to be more competitive. Otherwise, we enter a vicious circle. Therefore, the challenge is to ensure that, even before redistribution, there are fewer inequalities because many more people are working. Taking action upstream to repair less means entering a virtuous circle, and this obviously means allowing many more people to work, resulting in less income inequality before redistribution and, at the same time, increasing equality opportunities. More working people means more self-sufficient people, far fewer pockets of poverty, and many more socialised people, because work is one of the main forms of socialisation.

Let’s hope that these figures and findings, sometimes unexpected because they are little-known, like these analyses, will be able to contribute to a useful debate about the effective reforms to be conducted, without preconceptions or confusion between the ultimate objective of reducing inequalities, with a primary focus on the high inequality of opportunities in France, and the means to be used to achieve it. In the words of Bossuet: “God laughs at men who complain of the consequences while cherishing the causes”.

(1) On this topic, see Schumpeterian growth theory by Philippe Aghion.

(2) – The analysis of the cost of redistribution and the vicious circle created between income inequalities before and after redistribution and the lack of competitiveness of French companies was developed by Patrick Artus in several ‘economic flashes’.

The European League for Economic Cooperation-French section (ELEC-F) has organised a Citizens for Europe Consultation, approved by the ministry in charge of European Affairs, on the topic: “What improvements are desirable and realistic for the eurozone, from an economic and social point of view?”. This Consultation took place in two stages.

On 18 September, an initial meeting was held in order to pool the expectations, questions and proposals of the participants and to discuss them with three well-known economists: Agnès Benassy-Quere, Patrick Artus and Xavier Timbeau, as well as the President of ELEC-F, Olivier Klein. This debate was led by Emmanuel Cugny, editorial writer at France Info. Around 90 people participated.

On 16 October, a second meeting was held to summarise the conclusions and recommendations of this Consultation.

The two meetings were held in the BRED auditorium, 18 quai de la Rapée, 75012 Paris.

Summary : findings, proposals:

1. FINDINGS

The single currency

In the wake of Robert Schuman’s statement of 9 May 1950, the euro is one (and not the least) of these “concrete achievements which first create a de facto solidarity” that punctuate the construction of Europe. The 12 Signatory States of the Maastricht Treaty (1992) which took the major decisions, declared themselves “[determined] to promote economic and social progress […] through the establishment of economic and monetary union, ultimately including a single currency in accordance with the provisions of this Treaty”. Under the name of the euro, adopted in 1995, this single currency came into force in two stages, on 1 January 1999 and 1 January 2002, and the eurozone currently has 19 members. What is our view today on the usefulness of the euro and desirable improvements?

The single currency brings a basic economic benefit to its members by eliminating exchange fees between them. Above all, however, it eliminates exchange risk, facilitating the movement of capital and business within the zone. A second advantage is the sharp fall in interest rates brought about by the creation of the euro in many countries in the zone, be it through the effect of markets until 2010, or later through the action of the ECB. These lower rates facilitate business investment and reduce the burden of sovereign debt (government bonds in the financial market); without the euro, France’s public debt service, for example, would cost an additional €50 billion per year, or 2.5% of GDP. It should be noted, however, that the low interest rates experienced by some Southern countries prior to 2010 led to overindebtedness in the private sector.

It is also worth adding that, if the eurozone were a complete monetary zone as in the case of the United States for example, it would allow for differentiated growth rates within the same zone due to the coexistence of current account balances, some of which are in deficit and some of which are in surplus. In this kind of situation, countries with current account deficits would not be led to seek a lower growth rate than that corresponding to their needs (demographic needs for example). With an optimal organisation of the eurozone, the external constraint would only apply to the boundaries of the zone and not to the limits of each country forming it. From a consolidated point of view, the eurozone is currently one of the healthiest areas in the world in terms of its current account and public debt as well as enjoying a stable currency.

The usefulness of the euro has also been demonstrated in major recent upheavals the freezing of interbank loans after the collapse of Lehman Brothers and the recession caused by the severe financial crisis; the explosion of “spreads” on the public debts of Member States, the threat of deflation, etc. The single currency protected every country in the zone in 2008 and 2009; if each country had kept its own currency they would have certainly been weaker in the midst of the major financial crisis. The ECB has since been able to implement an extremely active, useful monetary policy. In addition, during the crisis specific to the eurozone, the institutional mechanism was expanded, in order to strengthen the resilience of the single currency, with the establishment of the Banking Union and the European Stability Mechanism.

As is demonstrated by the opinion polls in all member states, citizens currently see the benefits of the euro in a positive light, as the single currency not only facilitates travel but also more importantly offers protection. However, the advantages of the euro need to be highlighted and explained more effectively.

It would then be clearer to citizens that a complete eurozone could provide Europe with the capacity to act as a global player on the same levels as the United States with the dollar today and China with the yuan tomorrow. This renewed impetus at European level should also enable us to combat the effects of the extraterritoriality of American power. All in all, the citizens of each nation could therefore have more control over their own destiny.

Macroeconomic imbalances

“Convergence between European countries”, a major objective of successive treaties, was effective until the 2008 crisis, with the notable exception of the issue of current accounts. Since the crisis, however, it has been replaced by differences in living standards and a widening of macroeconomic imbalances between the member states of the eurozone Thus, after an initial period of convergence, the situation since the financial crisis specific to the euro zone is one of divergence between its Member States which is structural, cumbersome and multidimensional and which will inevitably take time to lessen.

One of the major difficulties is the lack of movement of capital between member states of the eurozone since 2010. Northern countries accumulate huge current account surpluses (currently amassed outside the eurozone more than within the zone) , but deposit all these savings outside the eurozone.

In the United States the private sector accounts for two-thirds of financial stabilisation (cross-capital flows between different States) with the remaining third being provided by the federal budget. The eurozone currently has neither.

This situation also reflects a geographical polarisation of production, which is concentrated in the northern countries and snowballs. Wage costs per unit produced have varied for a dozen or so years in a non-cooperative manner. Adjustments have therefore only affected southern countries in the form of “internal wage devaluations” and lower investment expenditure. These internal devaluations also have the collateral consequence of increasing actual debt (which is not devalued in parallel) and have had extremely problematic social and political repercussions. Salary re-evaluations in the northern countries are as yet in their infancy. Labour mobility is beneficial for northern countries but detrimental to those in the south. The divergent process is therefore cumulative.

Budgetary stability rules cannot be the only regulatory instruments applied in the monetary zone. In all events, they most certainly need to be simplified and revised. Structural convergence tools (structural funds) are abundant, poorly coordinated, ineffective and highly concentrated in non-eurozone countries. The European Stability Mechanism established in 2012 is an important non-monetary instrument in terms of guaranteeing financial support if a member state encounters an asymmetric shock. However, its working methods are felt to be too intrusive by beneficiary states and the European Parliament and are difficult to implement due to the established unanimity rule.

Overall these socio-economic divergences contribute to the mistrust of public opinion and the rise of sovereign populism. Europe must find the path towards upwards convergence. It needs to rediscover the real reasons behind this community of interest. Subsidiarity must not get in the way of interdependencies between member states, which fully justify interactive cooperation.

Northern countries have a long-term interest in maintaining solidarity with those in the south as, if producers were to continue to move significantly closer to purchasers, a large dynamic, sustainable European internal market would be a major asset and preferable to commercialism. In addition, and above all, a possible break-up of the eurozone would certainly have dramatic consequences for countries in difficulty but would lead to a major revaluation of the currencies of northern countries, which would considerably weaken their own economy.

2. OUR PROPOSALS

In our view, it is absolutely essential to maintain and consolidate the euro by completing the organisation of the eurozone:

The fundamental role of the ECB must be maintained as a lender of last resort in the event of systemic shocks in order to preserve the euro whatever it takes, while ensuring its stability.

Citizens of the European Union need to be aware that the European currency represents power and autonomy at world level against the US dollar and against the Chinese yuan in the future. The development of the role of the euro as an international currency against the dollar is to be recommended in order to move away as far as possible from the extraterritoriality of the laws of the United States.

The Banking Union needs to be consolidated: the aim is to finalise the resolution mechanism by implementing a safety net for public funds and introducing a common guarantee for bank deposits alongside the acceleration of provisioning of defaulting loans (classified NPLs) on the banks’ balance sheet.

We need to develop an IMF-type institution (based on the European Stability Mechanism), which can help countries in asymmetric balance of payments crises, without the creation of money.

In addition to this balance of payments risk management instrument, we need an actual cyclical stabilisation fund or a specific eurozone budget with a counter-cyclical and/or risk-sharing focus. This budget, which would be financed by own resources, would have to be put to the vote of a democratic institution, such as one stemming from the European Parliament. Further risk-sharing mechanisms may be possible within the eurozone which can take different forms (partially pooled unemployment insurance system, pooling of a proportion of public debt, etc.).

These risk-sharing systems must be conditional on the responsibility exercised by each country (structural reforms, budgetary situation, etc.). It is pointless to appeal for solidarity without responsibility. It should be pointed out, however, that whilst moral hazards must not be ignored, neither must they inhibit solidarity. A balance between these two principles needs to be obtained.

The return of capital mobility between eurozone countries is absolutely key so that the current account surpluses in certain countries can finance the deficits of others and encourage a healthy allocation of capital within the eurozone. The proposals outlined above should make a significant difference in this respect as they would restore the confidence of the financial markets in the unity and cohesion of the zone. We therefore need to pursue the course laid out by the Juncker Plan. The Capital Markets Union (CMU) should also be prioritised.

Surplus savings should be used to finance projects for the future (ecological transition, biotechnology, digital etc.) as well as to finance investment projects of this kind in southern countries. These could include public-private projects. This would also provide greater visibility and a better understanding of the usefulness of Europe.

In order to reduce the cumulative geographical polarisation of production systems and to encourage a cooperative development trend in all the member states of the eurozone, there is a need for a system which creates a productive rebalancing vision for the different areas within the eurozone to support the above-mentioned points and to rethink the instruments used (structural funds, incentives and private investment guarantees).

The current mechanism for monitoring macroeconomic divergences needs to be adapted particularly in terms of stepping up the monitoring of imbalances in current accounts and wage costs per unit produced. Greater emphasis needs to be placed on dialogue between social partners at eurozone level, in particular to avoid a social downward spiral.

3. CONCLUSION

It is important to highlight the benefits of the euro and the ways in which it protects citizens. It is also vital to stress that the single currency strengthens the bond within the zone and creates de facto solidarity. It is a means of promoting peace. The destruction of the euro would have severe consequences for Europe.

We therefore believe that it is necessary to promote an educational campaign, notably in the form of a dictionary of received ideas, in order to combat inaccurate or even malicious rumours which abound concerning the history and outcome of European construction.